译者 王为

文中黑字部分为原文,蓝字部分为译文,红字部分为译者注释或补充说明

COVID-19 Resurgences Will Keep Major Economies UnderPressure

by income genarator from seekingalpha.com

Summary

概要

-

The Invesco CurrencyShares Japanese Yen Trust (NYSEARCA:FXY) has fallen by more than 5% since March 9th, 2020.

-

Invesco基金公司管理的跟踪日元/美元汇率走势的交易所交易基金FXY的报价自2020年3月9日以来下跌了超过5%;

-

Resurgences of the COVID-19 pandemic could hit export growth by causing damage to global supply chains for the remainder of the year.

-

在今年剩余的时间里新冠疫情可能会给全球供应链体系带来损害并重创出口增长;

-

Long-term economic data suggest that significant vulnerabilities remain throughout the region and this could send FXY into the lower 80s during the next few months.

-

一些长期经济数据的表现说明亚洲地区的经济形势仍相当脆弱,并有可能导致FXY的报价在接下来的几个月里跌至81-84美元区间。

As 2020 has truly proven itself to be the yearof fiscal stimulus,government regulators in Japan are being forced to addressa resurgence ofthe COVID-19 epidemic. As a result of these events, markets remain on edgewithin the region and the Invesco CurrencyShares Japanese Yen Trust(NYSEARCA: FXY) has fallen by more than 5% since March9th. But while this is an instrument that is often associated with safe haven buying, there is little reason to believe that the tide will be turning anytime soon for investors holding long positions. Long-term economic data suggest that significant vulnerabilities remain throughout the region and this couldsend FXY into the lower 80s during the next few months.

事实证明2020年成了财政刺激手段频出的一年,面对卷土重来的新冠疫情日本政府高层正被迫苦寻对策。受这些事件影响,亚洲地区的金融市场仍紧绷神经,同时跟踪日元/美元汇率走势的交易所交易基金FXY的报价自2020年3月9日以来下跌了超过5%。虽然FXY经常被当做是一种避险资产,但几乎没有理由认为持有FXY多头仓位的投资者会在短期内见到新冠疫情的影响退去。长期经济数据的表现说明亚洲地区的经济形势仍相当脆弱,并有可能导致FXY的报价在未来几个月里处于刚刚超过80美元的水平上。

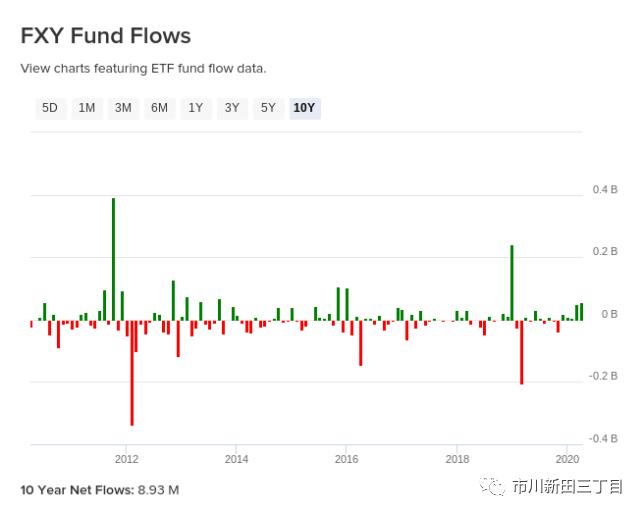

Source:ETFdb

Over the last decade, net flows that have directed toward FXY are nearly flat. Duringthis period we have seen wild fluctuations in volatility, with extremes being reached in 2011-2012, in 2016, and near the end of 2019. Aside from these periods, inflow volatility has been mostly subdued and this is why the netflows for the entire 10-year period have totaled less than $9 million. It should go without saying that this is a dismal inflow figure for such an extended period of time, so we can say that there were already significant challenges facing FXY even before the COVID-19 pandemic began to have a significant influence on global markets.

在过去十年里,FXY 基金申购赎回的资金量几乎持平。在此期间FXY 的规模经历了剧烈波动,最极端的资金进出情况出现在2011-2012期间,2016年以及2019年年底前后。在除此之外的其他时期里基金规模的变动幅度基本上都不大,这就是为什么整整十年过去后FXY的资金净流入量还不到9百万美元的原因。不言而喻,在如此之长的期间里资金净流入的规模才达到这个程度颇令人感到失望。因此可以这么认为,甚至在新冠疫情开始对全球金融市场产生大的影响之前,FXY基金就已经面临严峻的挑战了。

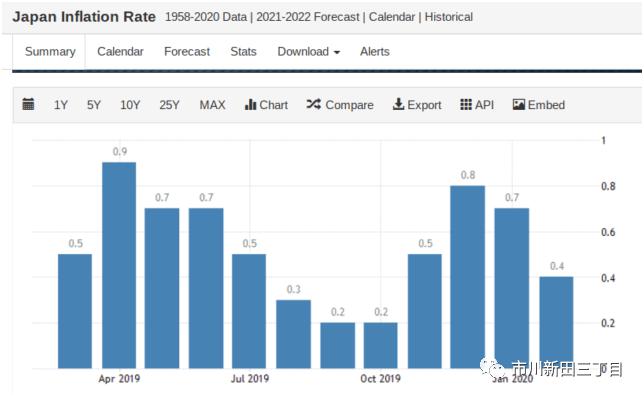

Source:Trading Economics

In February, consumer price inflation in Japan experienced a sharp drop to 0.4% (on an annualized basis). This was roughly half of what analysts were expecting and the slowest pace since October 2019. Core inflation figures (excluding food items) dropped from 0.8% to 0.6%. Areas of pronounced weakness were visible in electricity and water fees, education costs, and fuel prices, as these sectors continue to experience deflationary trends that have remained consistent for a fairly long period of time.

2020年2月份日本消费物价的增速大幅放缓至年化0.4%,几乎是分析师预测结果的一半,也是2019年10月以来的最低增幅。不包括食品类物价涨幅的核心通胀率从之前的0.8%跌至0.6%,物价涨幅明显趋弱的板块为水电费、教育支出、汽柴油费等,这些板块在相当长的期间里一直存在物价上涨乏力的问题。

Overall, these figures remain firmly below the Bank of Japan (BoJ) target inflation rate of 2% and this shows that the central bank is unlikely to find itself where an increase in interest rates would be appropriate any time soon. Ultimately, this means we are unlikely to encounter any significant market catalysts which might attract investors to yen-denominated assets during the remainder of this year.

总的来看,这些物价增长率仍远低于日本银行设定的2%的目标通胀率,说明日本银行不太可能在短期内做出加息的决策。说到底,在今年剩下的时间里不太可能在金融市场上看到任何足以令投资者对日元标价的金融资产感兴趣的重大事件。

Source:Trading Economics

Export figures out Japan are even more concerning because the country’s trade surplus is usually one of its standout features. Export figures have experienced drastic declines since last March and we expect that the negative effects of the COVID-19 pandemic will continue to put pressure on these areas of the economy. Sales declines have been apparent in Japan for the last 15 months, and we have already seen evidence that global health concerns will not only cause damage to global supply chains but to consumer demand levels, as well. Of course, there is nothing here that resembles a bullish economic environment, and so it will be difficult to see how these scenarios could inspire much buying activity in FXY over the next few months.

来自日本的出口数据甚至更令人感到担心,因为日本在对外贸易方面曾长期处于顺差状态。但自2019年3月以来,日本的出口经历了大幅下挫,我们预测新冠疫情带来的负面影响将继续施压日本经济中与出口有关的板块。在过去15个月中,日本对外销售额的下降幅度相当明显,已经看到一些证据显示全球范围内对健康问题的担忧将不仅对全球供应链的运营而且也会对消费端的需求产生不利影响。当然了,由于经济大环境看上去没有走强的迹象,因此很难想象这样的经济前景会在未来几个月里给FXY基金带来多少买盘。

Source:Author, TradingView

From the technical viewpoint, we have identified two important price support levels that could work as viable price targets in FXY over the next few months. The first price support level can be found near the lows from the end of 2019 (at 83.70). If prices extend beyond this support level, the next price target could be found near the lows from the end of 2017 (at 81.40). Of course, these levels suggest potential declines of nearly 8% relative to current levels, so it looks as though FXY still has further to fall before investors can hope for any sort of real stabilization.

技术分析方面,可以看到有两个重要的支持位会在未来几个月里起到支撑作用。第一个支持位在2019年末的低点83.70附近,如果继续向下突破,下一个支持位位于2017年末的低点81.40附近。81.40要比当前的价位低8%左右,因此FXY基金在真正企稳之前似乎仍有继续下跌的空间。