撰稿人 / 桑之未

洞察中国豪华车市场

报道 | 数据 | 咨询

(This article is attached with English translation)

【关键词】豪华车市场终端销量、市场份额、经销商新车利润

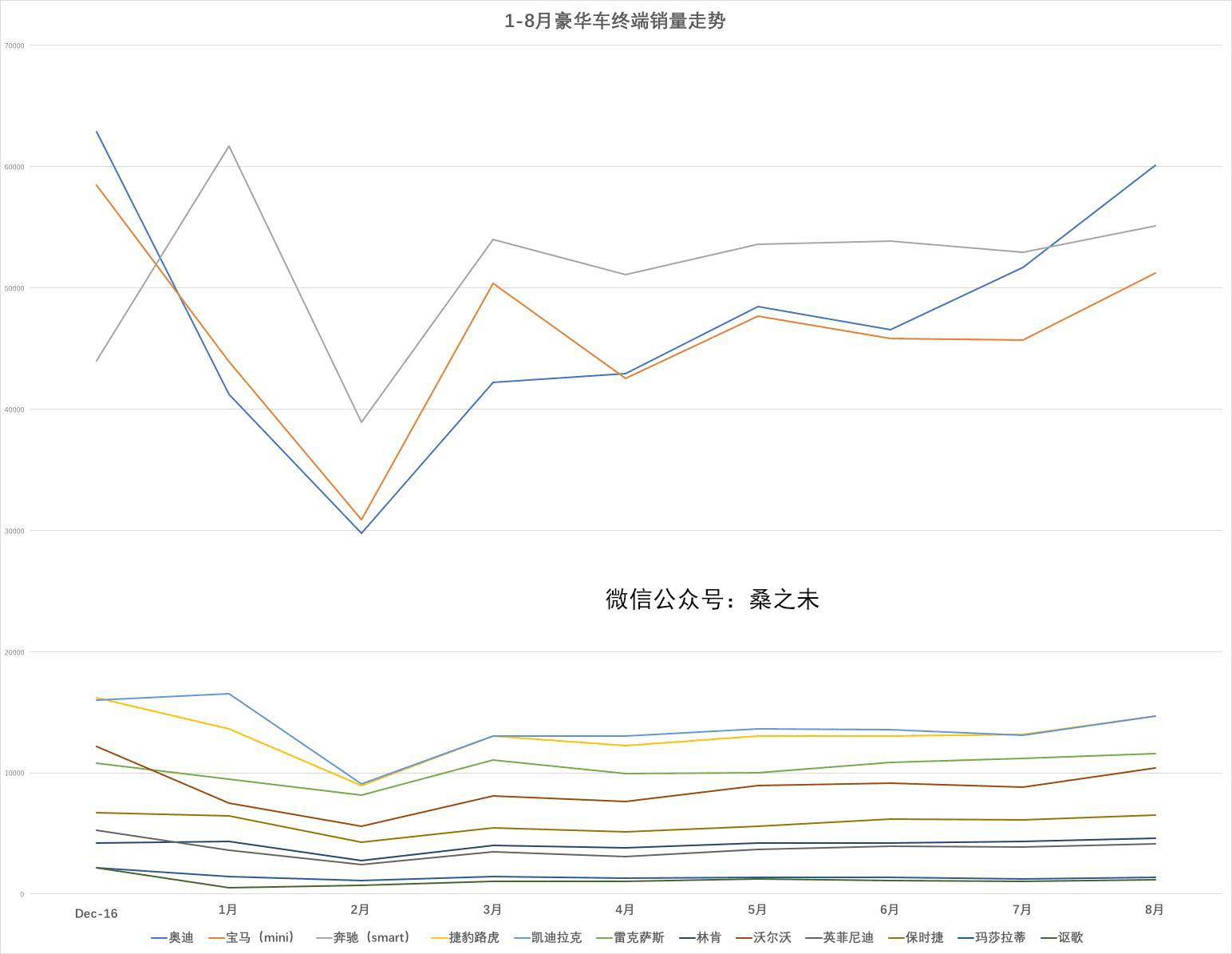

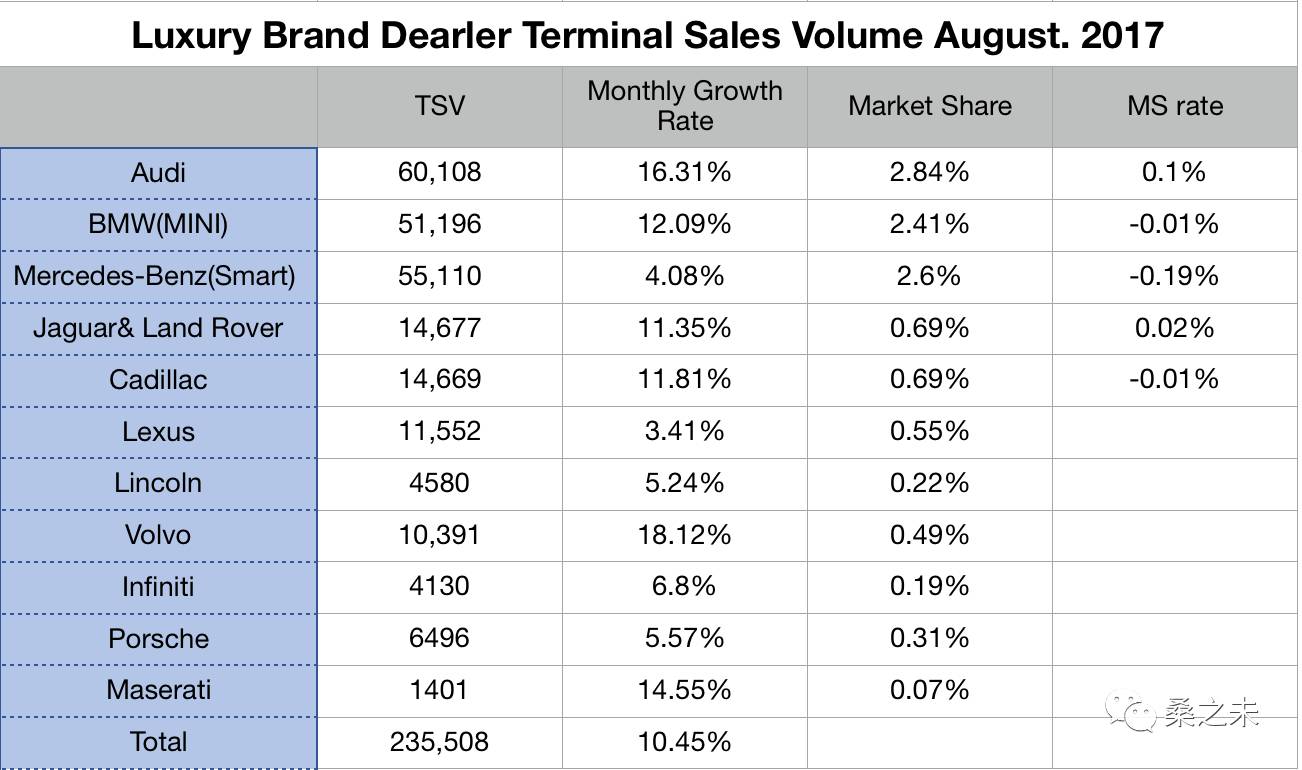

2017年8月12个豪华车品牌官方公布的销量1-8月累计销量为1,632,634辆,同比增长18.9%;1-8月经销商终端零售累计销量为1,623,690辆同比增长18.8%。其中8月经销商终端零售数量为235,508辆增环比增长10.45%; 8月份豪华车市场持续向好,销商终端零售销量环比增长超过10%的品牌有,奥迪、宝马、凯迪拉克、捷豹路虎、沃尔沃、玛莎拉蒂等。

1-8月豪华车终端销量走势

奔驰

奔驰(含smart、福奔)8月经销商终端零售数量为55,110辆环比增长4.08%,市场份额2.6%,份额增长-0.19%,经销商库存在1.0以下。奔驰经销商8月份新车利润环比下滑16.51%。8月份奔驰经销商清理旧款C级,准备切换小改款C级,这导致经销商新车利润环比有所下降。ABB在8月加大了这个级别车型市场的销售力度,奔驰C级、宝马3系、奥迪A4L三款车型销量合计环比增加9%,其中奥迪A4L销量环比增加20.3%为1.25万辆。奔驰其他主力销售车型,经销商利润变化不大,奔驰E级微降,GLC经销商新车利润同比下滑5.13%。奔驰经销商第四季度销售任务压力不大,估计销量会进一步压缩,利润进一步提升。

宝马

宝马(MINI)8月经销商终端零售数量为51,196辆环比增长12.09%,市场份额2.41%,份额增长-0.01%,经销商利润环比下滑。宝马连续两个月官方销量低于销商终端零售数量,可以看到,这两个月经销商库存、抄报得以降低,经销商压力进一步释放。宝马7月重启“BMW X之旅”市场活动得以见效,8月宝马X系列车型终端零售销量突破1.8万辆环比增长13.3%,其中宝马X1终端零售销量环比增长15.05%、宝马X3增长13.48%、宝马X5增长4.85%,宝马X5是这个级别的销量冠军销量达4500辆。宝马经销商目前的问题是主力车型不盈利,宝马5系销量急需爬升到1万辆。

奥迪

奥迪8月经销商终端零售数量为60,108辆环比增长16.31%,市场份额2.84%,份额增长0.1%,奥迪在8月份市场份额已经超过奔驰,跃居8月豪华车市占率第一,1-8月累计计算奔驰市场分额仍然排名第一。8月奥迪三款车型终端零售超过1万辆,其中奥迪A6L经销商终端零售创纪录销售出1.47万辆环比增长14.32%;奥迪A4L销量为1.25万辆增长20.3%,奥迪Q5销量为1.19万辆增长9.49%,奥迪A3增长17.75%。8月奥迪主销车型销量大幅度提升,同时经销商利润也出现下滑,部分地区经销商利润环比下滑50%。奥迪经销商剩下4个月要完成近24万辆的销量目标,经营压力比较大。

凯迪拉克

凯迪拉克8月经销商终端零售数量为14,669辆环比增长11.81%,市场份额0.69%,份额增长-0.01%;凯迪拉克主力销售车型ATS-L八月经销商终端销量为5078辆环比增长9.53%,厂家对经销商补贴力度也非常大,达到28.19%,在这个级别中也是厂家补贴力度最大的。XT5八月销量为5005辆销售折扣在16%左右。8月凯迪拉克经销商新车利润环比下滑。

捷豹路虎

捷豹路虎8月经销商终端零售数量为14,677辆环比增长11.35%,市场份额0.69%,份额增长0.02%。路虎品牌经销商新车利润处在盈亏线上下,捷豹品牌新车利润为负;8月国产发现神行返利增加经销商利润得以改善,销量环比增加13.88%,新车利润环比增加40%左右。国产XFL八月经销商终端零售环比增加17.53%,但新车优惠也增至23.6%左右。揽胜以及揽胜运动两款车型经销商终端销量分别接近2000辆,经销商有1-2个点的新车利润。

雷克萨斯

雷克萨斯 8月经销商终端零售数量为11,552辆环比增长3.41%,市场份额0.55%,经销商利润接近5%。ES是雷克萨斯主力销售车型,8月零售终端销量5219辆增长4.67%,经销商保持合理的利润。RX本月销量增长11.54%,这款车型经销商新车9个点左右的利润。NX减少了供应,经销商新车利润回升。

沃尔沃

沃尔沃8月经销商终端零售数量为10,391辆环比增长18.12%,市场份额0.49%,经销商利润不算好。沃尔沃销量提升受益于国产S60L、S90、XC60以及进口XC90销量的提升。沃尔沃S60L市场折扣在27%左右,S90市场折扣在15%左右,XC60市场折扣在24%左右,进口XC90市场折扣在19%左右,沃尔沃厂家对经销商返利支持力度也大,在21%上下,沃尔沃产品定价高,品牌力弱,是今后需要解决的问题。

保时捷

保时捷8月经销商终端零售数量为6496辆环比增5.57%,市场份额0.31%,经销商库存1.92。保时捷两款SUV卡宴、Macan八月经销商终端零售合计近5000辆,销量占比76.2%,新款PANAMERA月销接近1000辆,占比13.9%,改款后受到消费者欢迎,成为又一款经销商收获利润的车型。

林肯

林肯8月经销商终端零售数量为4580辆环比增5.24%,市场份额0.22%。林肯厂家在8月对经销商的返利支持力度增加1.2%,其中MKC、MKX支持力度加大,零售折扣增加带动销量提升,其中MKC终端销量环比增长5.64%达1480辆,MKX环比增长12.08%达1058辆。林肯今年的商务政策比较灵活,跟随市场节奏不断调整,经销商新车利润得以保证。

英菲尼迪

英菲尼迪8月经销商终端零售数量为4130辆环比增6.8%,市场份额0.19%,经销商整体单车利润环比有所转好。英菲尼迪8月加大了Q50L、Q70L返利支持力度,国产车型Q50L经销商终端零售销量增长11.2%达到1856辆,*口车进**型Q70L增长16.81%达667辆,国产车型利润不是很理想处在亏损状态。

玛莎拉蒂

玛莎拉蒂8月经销商终端零售数量为1401辆环比增14.55%,市场份额0.07%,经销商库存1.85,处在高位。

文中涉及的数据,多是从国内经销商集团调研而来的数据,其中文中提及的“单车利润”是指经销商销售新车时赚取的利润,数据涉及单车加权平均销售价格、厂家返利(包含固定返利、考核奖励、促销补贴、人员奖励等),销售折扣等;这里不包含衍生精品的销售利润;“库存系数”是指当月销量除以过去三个月销量均值。

版权声明:本文系@桑之未 #原创首发# 转载或改编请与本人沟通,如有任何侵权行为,侵权者将承担相应的法律责任。汽车行业人士留言可以索取本人微信号码,更多行业信息查阅朋友圈分享内容。2017-09-29 北京

▪ 往期精彩阅读 | More Reading ▪

— — 中英文分割线 — —

The Retail of Luxury Car Dealers Increases by 10.45% on Month-on-month Basis, and the Sales Volume of Audi Exceeds 60,000 Vehicles for the First Time

Written by / Sangzhiwei

Insight into the Chinese Luxury Car Market

Report | Data | Consulting

Keywords: Terminal sales volume of luxury brand market, market share, and profit of dealer

In August 2017, the officially announced accumulative sales volume of 12 luxury brands from January to August was 1,632,634, an increase of 18.9% YoY. From January to August the accumulative sales volume of terminal retail of dealers was 1,623,690, an increase of 18.9% YoY. Among them, in August the terminal retail volume of dealers was 235,508, an increase of 10.45% month over month. The luxury car market continued to grow in August. Brands with over 10% growth of terminal retail volume includes Audi, BMW, Cadillac, Jaguar Land Rover, Volvo, Maserati, etc.

Mercedes-Benz

In August the terminal retail volume of Mercedes-Benz dealers (including Smart and Fujian Benz) was 55,110, an increase of 4.08% month over month. The market share was 2.6%, up by -0.19%. The dealer inventory was below 1.0. The new car profit of Mercedes-Benz dealers fell by 16.51% month over month. In August Mercedes-Benz dealers was clearing the old C-Class and would switch to the small modified new C-Class, resulting in reduction of new car profit of dealers month over month. In August ABB intensified the efforts on sales in the market of B class (large family car). The total sales volume of Mercedes-Benz C-class, BMW 3 Series and Audi A4L increased by 9% month over month. Among them, the sales volume of Audi A4L was 12,500, an increase of 20.3% month over month. Profit of dealers of other main sales models of Mercedes-Benz had little change. Profit of dealers of Mercedes-Benz E-class dropped slightly. The new car profit of dealers of GLC fell by 5.13% month over month. In the fourth quarter, there will be only little sales target pressure on Mercedes-Benz dealers. It could be estimated that sales volume will further decrease and profits will further increase.

BMW

In August the terminal retail volume of dealers of BMW (MINI) was 51,196, an increase of 12.09% month over month. The market share was 2.41%, up by -0.01%. The profit of dealers dropped month over month. The official sales volume of BMW was less than the terminal retail volume of dealers for two consecutive months. It can be seen that in these two months the dealer inventory and over-reporting reduced, and dealers’ pressure was further released. In July "BMW X Trip" market activity restarted by BMW was effective. In August the terminal retail sales volume of BMW X Series was more than 18,000, an increase of 13.3% month over month. Among them, the terminal retail sales volume of BMW X1 increased by 15.05% month over month and that of BMW X3 increased by 13.48%, and that of BMW X5 increased by 4.85%. BMW X5 was the sales champion in this class, whose sales volume was 4,500. The current issue for BMW dealers is the profitless of main models. The sales volume of BMW 5 Series needs to climb to 10,000 urgently.

Audi

In August the terminal retail volume of dealers of Audi was 60,108, an increase of 16.31% month over month. The market share was 2.84%, up by 0.1%. Audi’s market share had exceeded Mercedes-Benz in August. Its market share in luxury brand was Top 1 in August. The accumulative market share from January to August of Mercedes-Benz still ranked the first. In August the terminal retail volume of three Audi models exceeded 10,000. Among them, the terminal retail volume of Audi A6L set a new record of 14,700, an increase of 14.32% month over month. The sales volume of Audi A4L was 12.500, an increase of 20.3%. The sales volume of Audi Q5 was 11,900, an increase of 9.49%. The sales volume of Audi A3 increased by 17.75%. In August the sales volume of main models of Audi increased significantly. At the same time, the profit of dealers also fell. In some areas, the profit of dealers fell by 50% month over month.. With 4 months left this year, Audi dealers will achieve the sales target of nearly 240,000. The operating pressure is relatively big.

Cadillac

In August the terminal retail volume of dealers of Cadillac was 14,669, an increase of 11.81% month over month. The market share was 0.69%, up by - 0.01%. In August the terminal sales volume of dealers of ATS-L, the main sales model of Cadillac, was 5,078, an increase of 9.53% month over month. The manufacturer’s subsidies for dealers were as high as 28.19%. The manufacturer’s subsidies of this class is the highest. The sales volume of XT5 in August was 5,005, and the sales discount was about 16%. In August the new car profit of dealers of Cadillac dropped month over month.

Jaguar Land Rover

In August the terminal retail volume of dealers of Jaguar Land Rover is 14,677, an increase of 11.35% month over month. The market share was 0.69%, up by 0.02%. The new car profit of dealers of Land Rover brand was around bottom line, and the new car profit of Jaguar brand was negative. In August domestic SE increased rebate and improved dealers’ profit. The sales volume increased by 13.88% month over month. The new car profit increased around 40% YoY. In August the terminal retail of dealers of domestic XFL increased by 17.53% month over month, but the discount of new car also increased to around 23.6%. The terminal sales volume of dealers of Range and Range Rover Sport was nearly 2,000. The new car profit of dealers was 1%-2%.

Lexus

In August the terminal retail volume of dealers of Lexus was 11,552, an increase of 3.41% month over month. The market share was 0.55%. The profit of dealers was close to 5%. ES was the main sales model of Lexus. In August the retail terminal sales volume was 5,219, an increase of 4.67%. Dealers maintained a reasonable profit. The sales growth of RX this month was 11.54%. The new car profit of dealers for this model was 9%. NX reduced supplies, and the profit of new car of dealers rebound.

Volvo

In August the terminal retail volume of dealers of Volvo was 10,391, increase of 18.12% month over month. The market share was 0.49%, and profit of dealers was not well. The increase of sales volume of Volvo benefited from the increase of sales volume of domestic S60L, S90, XC60 and imported XC90. The discount of Volvo S60L market was around 27%, the discount of S90 market was around 15%, the discount of XC60 market was around 24%, and the discount of imported XC90 market was around 19%. Volvo manufacturer’s rebate support to dealers was around 21%, which was big. Volvo has a high product pricing and weak brand strength, which needs to be solved in future.

Porsche

In August the terminal retail volume of dealers of Porsche was 6,496, an increase of 5.57% month over month.The market share was 0.31%, and dealers’ inventory was 1.92. The total terminal retail of dealers in August of Cayenne and Macan, two SUVs of Porsche, was nearly 5,000. The sales volume accounted for 76.2%. The monthly sales volume of new Panamera was close to 1,000, accounting for 13.9%. After modification, it was well welcomed by customers, and became another profitable model for dealers.

Lincoln

In August the terminal retail volume of dealers of Lincoln was 4,580, an increase of 5.24% month over month. The market share was 0.22%. In August Lincoln manufacturer’s support to the dealer rebate increased by 1.2%. Among them, the support to MKC and MKX increases significantly. The increase of retail discount drove the sales promotion. The terminal sales volume of MKC increased by 5.64% to 1,480 month over month. And that of MKX increased by 12.08% to 1,058 month over month. This year, Lincoln’s business policy was relatively flexible, and constantly adjusted according to the market rhythm. The new car profit of dealers was guaranteed.

Infiniti

In August the terminal retail volume of dealers of Infiniti was 4,130, an increase of 6.8% month over month. The market share was 0.19%. The unit profit of dealers increased month over month. In August Infiniti increased rebate support to Q50L and Q70L. The terminal retail sales volume of dealers of domestic model Q50L increased by 11.2% to 1,856. That of imported Q70L increased by 16.81% to 667. The profit of domestic model was not ideal, and was in a state of loss.

Maserati

In August, the terminal retail volume of dealers of Maserati was 1,401, an increase of 14.55% month over month. The market share was 0.07%. The dealers’ inventory coefficient stayed at a high level of 1.85.

Copyright statement:This article is anoriginal article published by Sang Zhiwei for the first time. For reproduction or adapting, please communicate with the author. In case of any infringement, the infringer will bear the corresponding legal responsibilities. Readers in the auto industry can leave a message and ask for the author’s personal WeChat number. For more information of the industry, refer to the content shared in Circle of Friends. September 29th, 2017, Beijing.

▪ ▪ ▪ MORE READING ▪ ▪ ▪