译者 王为

文中黑字部分为原文,蓝字部分为译文,红字部分为译者注释或补充说明

Interest Rates Gaps for the US Dollar

By Erik Norland

Interest rate differentials between currencies can be crucial in foreign exchange markets for pricing purposes such as in the carry trade, and they have taken on added significance with the advent of negative rates in Europe and Japan over the past few years. So, how big are the interest rate differentials between currency pairs? On the face of it, it seems like a simple enough question. But the variety of ways used to measure the differential makes for a complicated answer. Differences in rates between central banks can be used as a guide but may be of limited value to everyday currency traders as only major financial institutions deal directly with central banks.

在外汇市场上,各货币之间的利差对于汇率的定价至关重要,比如在利差交易中,过去几年中随着负利率在欧洲和日本开始兴起,利差对于汇率定价的影响日渐增强。那么,不同货币对之间的利差会大到什么程度呢?乍一看,这个问题似乎不难回答,但由于利差水平的计算方法不止一个,回答这个问题并非那么轻而易举。各国央行官方利率之间的利差也许可以拿来作为各货币之间利差水平的标杆,但其对外汇交易员的日常交易来讲参考作用似乎有限,因为只有大的金融机构才能直接与央行做交易。

In financial theory, market participants would typically look at interbank rates, such as ICE LIBOR, as a guide. Unlike the official central bank rate, interbank rates offer a look at private sector lending rates. However, these rates may not reflect the rate differentials that currency traders are actually getting in the market. Also, the rates have been discontinued for several currencies.

金融理论认为,市场参与者通常以银行间的利率比如美国洲际交易所公布的LIBOR利率作为定价基准。与央行公布的官方利率不同之处在于,银行间利率反应的是私营金融机构之间相互借贷资金的成本。但是,这些银行间利率的水平可能并没有真正体现出外汇市场上实际交易所产生的利差水平。况且,有几个货币的银行间利率的报价已经终止了。

Overnight index swap rates (OIS) such as EONIA can also be used to gauge the level of interest differentials among currencies. OIS rates, however, stick closely to central bank rates and may also not fully reflect the interest rate gaps currency investors are getting in the market.

像欧元隔夜拆放利率均值指数EONIA这样的隔夜拆放指数互换利率也可被用来作为衡量各货币间利差水平的指标,但是这些利率的走势通常紧跟央行的利率变化,也无法完美体现外汇市场利差的实际水平。

Another avenue for calculating interest rate differentials is the currency market itself, where implied interest rate differentials can be calculated from the difference in the value of a currency in the spot and futures markets. For example, CME’s FX Swap Rate Monitor calculates the implied interest rate differential between CME FX futures and CME FX Link’s central limit order book (Figure 1).

另一个测算利差水平的方法来自外汇市场本身,外汇市场隐含的利差水平可通过即期汇率和远期汇率之间的汇差推算出来。例如,在芝加哥商品交易所外汇互换利率行情界面上显示的就是芝加哥商品交易所外汇期货合约的报价与芝加哥商品交易所外汇直联交易板块的外汇即期报价之间的汇差隐含的利差,见图1。

Figure 1: FX markets shows larger interest rate differentials than other measures

外汇市场隐含的美元对其他货币的利差要高于其他方式推算出来的结果

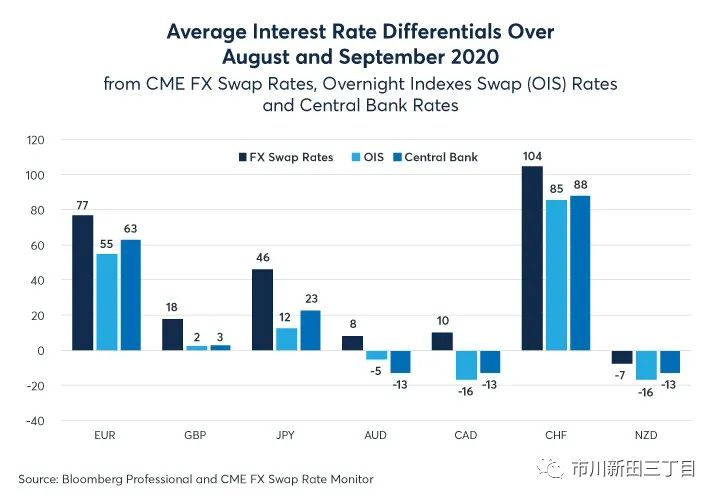

What’s curious is that when these ways of measuring interest rate differentials are compared, the currency market measure consistently showed a larger interest rate gap between the US rate and the foreign currency rate than did central bank rates or the OIS. In other words, US interest rates appeared higher relative to other countries when observed in the currency market than in the interest rates market. This was true across seven different currencies on CME FX Swap Rate Monitor measured over August and September. Some of these gaps were as big as 20 or 30 basis points. This is to say that US dollar rates appear to be relatively higher versus rates in Australia, Canada, the eurozone, Japan, New Zealand and Switzerland than the differences from central bank rates or OIS would suggest.

有意思的是在对各种利差计算方法的结果进行比较时可以发现,通过即远期汇率之间的汇差折算出来的美元和其他货币之间的利差水平通常与美国和其他国家央行利率之间以及美国和其他国家的隔夜拆放指数互换利率之间的利差水平相距甚远。换言之,外汇市场隐含的美元与其他国家货币之间的利差水平似乎要高于利率市场上的利差水平,芝加哥商品交易所外汇互换利率行情界面8、9两月份对美元与7个主要货币之间的利差测算结果证明了这一点。这些利差水平之间的差异有时会高达20-30个基本点,也就是说,美元利率与澳大利亚、加拿大、欧元区、日本、新西兰以及瑞士利率之间的利差要高于央行间利率以及隔夜拆放指数互换利率之间的利差。

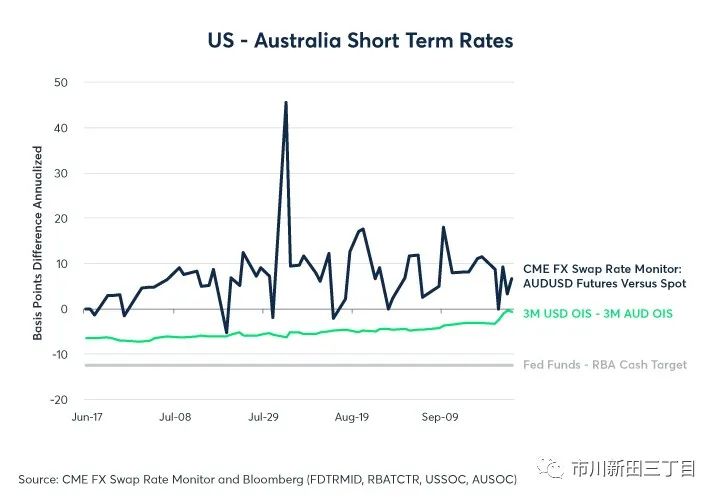

For some currencies, like the Australian (AUD) and New Zealand dollars (NZD), the gap between the currency market and the OIS rate differentials are fairly small, averaging around 10 basis points (bps). For most of the other currencies, the gap is more substantial, averaging around 20-25bps for the euro (EUR), British pound (GBP), Canadian dollar (CAD) and Swiss franc (CHF). For the Japanese yen (JPY), the rate gap between the currency market and the OIS measures has been larger (around 35 bps). In every case the currency market measure shows US rates being higher relative to the other countries when compared to the central bank rate or OIS measures.

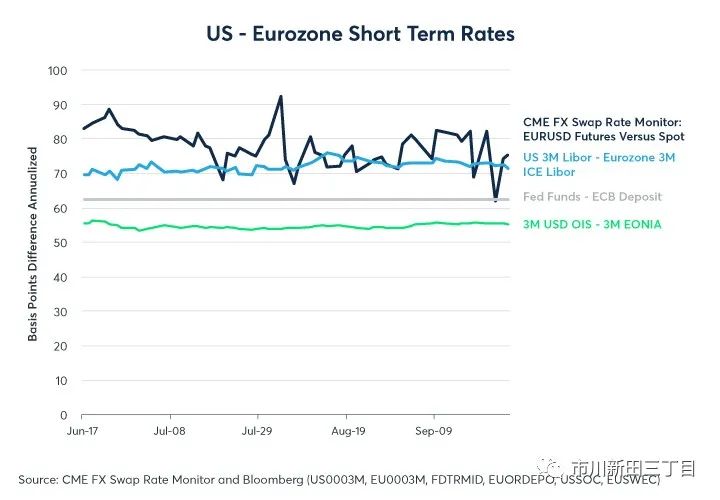

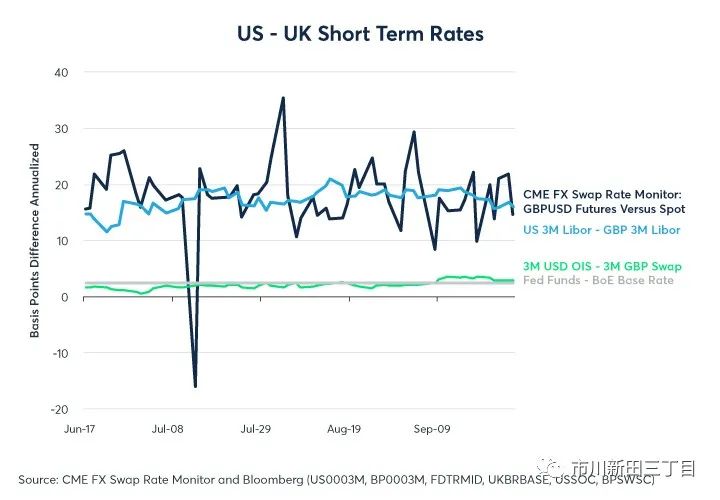

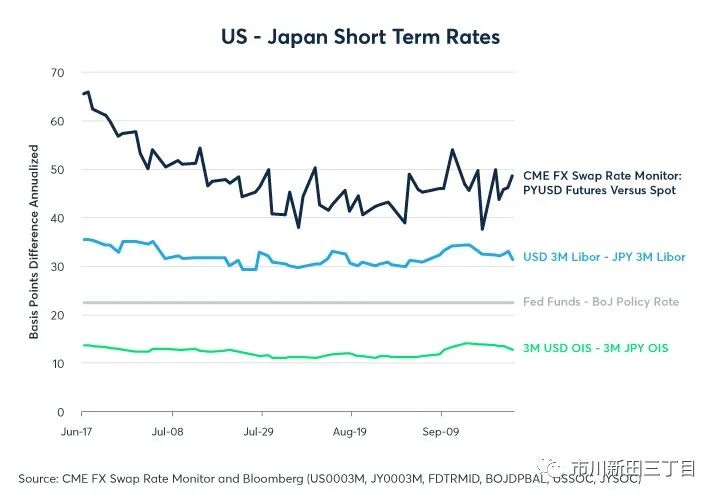

对于某些货币比如澳大利亚元以及新西兰元来讲,外汇市场隐含的利差与通过隔夜拆放指数互换利率的水平推算出来的利差之间的差距要小很多,平均为10个基本点左右。而对于其他大多数货币来讲,这个差距就要大很多了,这两个方式测算出来的美元与欧元、英镑、加拿大元和瑞士法郎之间的利差之间的差异均值约为20-25个基本点。而美元和日元之间的外汇市场隐含的利差与隔夜拆放指数互换利率的利差之间的差异更大,为35个基本点。不管对于哪个货币对来讲,外汇市场所隐含的美元与其他货币之间的利差均大于央行利率之间以及隔夜拆放指数互换利率之间的利差。

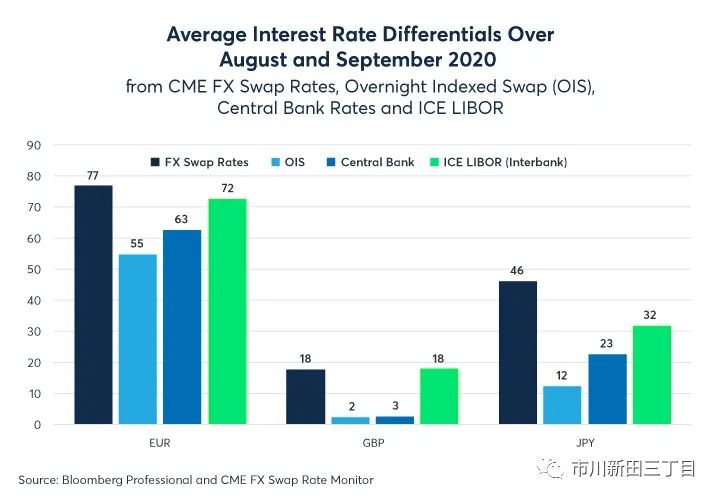

For EUR, GBP and JPY, the interbank (ICE LIBOR) rate measure is closer to the FX Currency Swap Monitor measure. Even here, however, the currency futures market measure shows that the EUR-USD interest rate differentials were, one average, 5 bps greater than the interbank measure and 14 bps greater in Japan. By contrast, for the UK, those two values have been in line over the past two months (Figure 2).

对于欧元、英镑和日元来讲,通过银行间利率(以美国洲际交易所公布的LIBOR利率为代表)的水平测算出的美元对这三个货币的利差与芝加哥商品交易所外汇互换利率行情显示界面测算的结果差异很小。即便如此,通过外汇期货合约报价折算出来的欧元/美元和美元/日元的利差平均要比银行间利率之间的利差分别高5和14个基本点。与此形成鲜明对比的是,通过这两个方法测算出来的英镑/美元的利差在过去两个月里保持了一致,见图2。

Figure 2: OIS comes close but still shows smaller rate differentials than FX markets

隔夜拆放指数互换利率之间的利差与外汇市场隐含的利差水平差距不大,但仍有一点差距

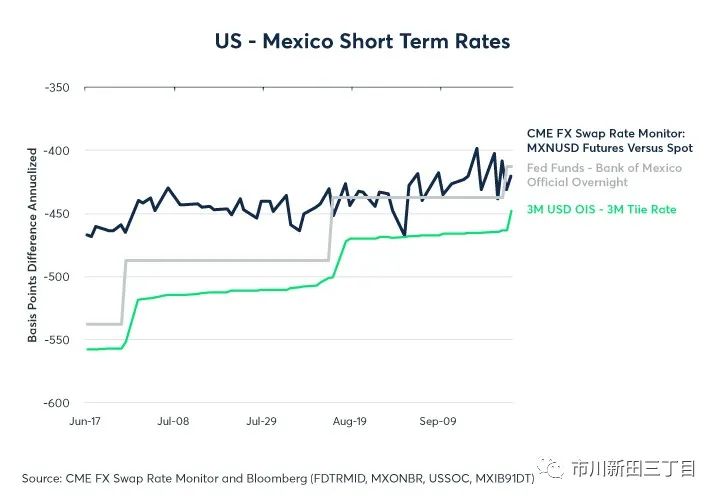

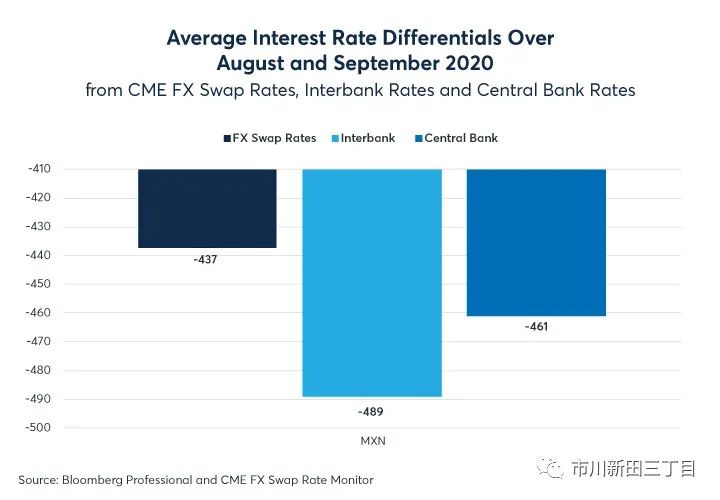

The seven currencies mentioned share one thing in common with the US dollar: they all have official central bank rates near zero. Among the currencies on CME’s FX Swap Rate Monitor, only the Mexican peso has interest rates substantially above zero – in the 4-5% range. For the Mexican peso as well, the currency market measure showed US rates on average 50 bps higher relative to Mexican rates than is the case in the OIS market and about 24 bps higher than the two nations’ central-bank rates would suggest (Figure 3). This difference probably arose from the fact that the Mexican central bank cut rates twice over the past two months which was anticipated by the currency forward markets but not by overnight swap rates.

前面提到的七个货币与美元之间存在一个共同点:这些货币的央行官方利率均接近0。在芝加哥商品交易所的外汇互换利率行情显示界面上公布的各货币中,只有墨西哥比索的官方利率明显高于0,处于4%-5%的区间范围内。同样对于墨西哥比索来讲,外汇市场所隐含的美元对墨西哥比索的利差仍比美墨隔夜拆放指数互换利率之间的利差高50个基本点,比两国央行利率之间的利差高24个基本点,见图3。这个差异可能与墨西哥央行在过去两个月里两次降息有关,这两次降息行动被外汇市场提前预测到并在远期汇率的报价中体现了出来,而隔夜拆放指数互换利率却没有做到先知先觉。

Figure 3: In Mexico, too, USD rates appear higher than they do for the other currencies

即使是高利率的墨西哥比索,外汇市场隐含的美元与墨西哥比索之间的利差水平仍高于其他方式推算的结果

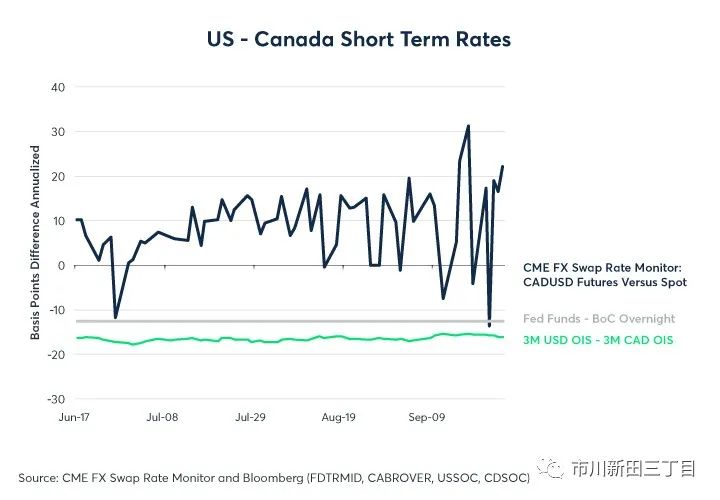

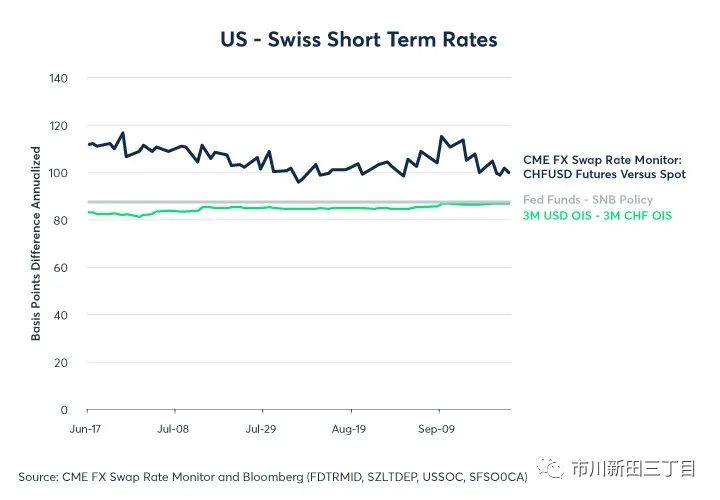

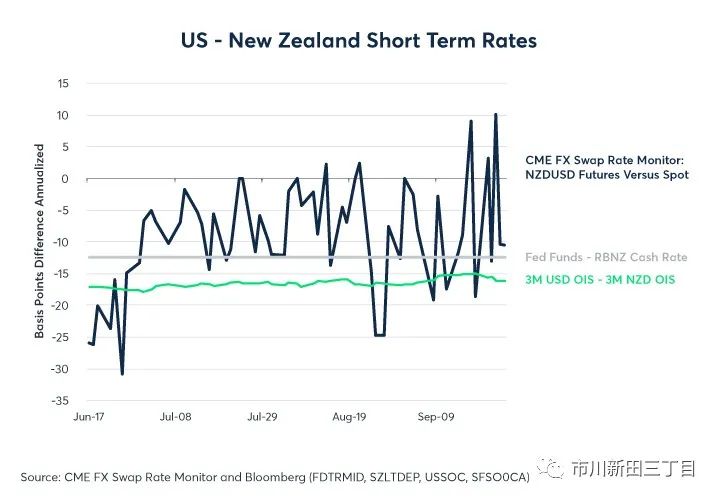

As one can see in the appendix (Figures 4-11), the day-to-day values are a bit choppier than the averages, but even so, the currency market mostly shows a greater gap than the other measures. So, this begs the question: Why would the currency market imply that US rates are higher relative to other country’s rates so consistently and across so many currencies than would be implied from the differentials calculated from interbank or central bank rates?

如下图4-图11所示,各交易日美元与各货币之间的利差要比均值的波动范围大一些,但即使如此,通过即远期外汇汇率之间的汇差推算出来的利差水平大多要比通过其他方式计算得出的利差要高。那么,问题来了:为啥外汇市场隐含的美元对这些货币的利差水平会一直高于其他方式得出来的利差,比如银行间利率之间的利差以及各国央行官方利率之间的利差,为啥这种现象出现在如此之多的货币身上?

One answer is that the relatively higher US rates implied in the currency markets might reflect a global forward demand for U.S. dollars. In certain cases, like in Japan and the UK, it might also reflect expectations that their central banks may soon be lowering interest rates. That said, if that expectation does exist, it should, in theory, also exist in the interbank rates but should only be seen in the OIS market in the 24 hours before a rate move.

有一种解读认为,外汇市场隐含的美元利率水平之所以偏高可能体现的是全球未来对美元的需求状况。在某些情况下,比如日本和英国,这种现象也许意味着市场预期这两家央行可能很快就将下调官方利率的水平。从理论上讲,即使这种预期确实存在的话,也应体现在银行间利率的定价上,但仅在利率下调之前24小时的隔夜拆放指数互换利率市场上方可显示出来。

One thing is clear, those who trade in the currency markets and those who work in short-term interest markets might want to keep a close eye on the interest rate differentials implied between currency futures and the spot FX market as an additional reference point in their trades.

有一点是清楚的,在外汇市场上的交易者和短期利率市场的参与者可能需要在做交易的同时密切关注外汇即期汇率的报价以及外汇期货合约报价之间的汇差所隐含的利差水平。

Figure 4: EURUSD Rate Differentials

Figure 5: GPDUSD Rate Differentials

Figure 6: JPYUSD Rate Differentials

Figure 7: AUDUSD Rate Differentials

Figure 8: CADUSD Rate Differentials

Figure 9: CHFUSD Rate Differentials

Figure 10: NZDUSD Rate Differentials

Figure 11: MXNUSD Rate Differentials