本文首发于智堡公众号:zhi666bao。

原标题:迷失于传导 Lost in Transmission

本文由Mikko翻译,仅供学习使用(原报告已经处于公开分享状态),作者Zoltan Pozsar在不久前的彭博的Podcast节目中深度分析了美债持有者结构变迁的原因,此为其深度报告的译文。

There’s something wrong with prices in funding and bond markets currently.

目前融资市场和债市价格存在问题。

The net supply of U.S. Treasuries will increase by over $1 trillion this year, and foreign FX hedged buyers will have to buy a large portion of this supply. But the curve is currently inverted relative to hedging costs, and foreigners won’t increase purchases unless the curve re-steepens relative to FX hedging costs.

今年,美国国债的净供应将增加1万亿美元以上,外国的外汇风险对冲的买家将不得不购买这一供应的很大一部分。但相较于对冲成本(的曲线),国债收益率曲线处于倒挂状态,除非国债收益率曲线相对于外汇对冲成本得以重新陡峭化,否则海外投资者不会增加购买量。

The required adjustments are huge – at least 100 bps.

但所需的国债收益率曲线调整是巨大的——至少100个基点(陡峭化)。

For the 10-year to be attractive relative to other G7 bonds on a hedged basis, yields would have to back up to at least 3.5% and more realistically to 4.0%; alternatively, three-month FX hedging costs would have to come down to 2.0%, either through positive cross-currency bases, much lower bill yields or rate cuts.

在外汇对冲的基础上,10年期国债要相对于其他G7债券具备吸引力,收益率必须至少回升到3.5%,甚至4%更切合实际;另外,三个月期的外汇对冲成本将不得不降低到2%,或通过交叉货币互换基点的走正、大幅降低的短期国债收益率,要么就是联储降息。

Yet markets do not expect any of this for 2019.

然而,市场预计2019年不会出现这种情况。

First, the market expects the 10-year yield to stay roughly at its current level; second, the market expects core cross-currency bases to widen, not tighten; third, the market expects Libor-OIS spreads to tighten, but only marginally; and fourth, the market does not expect either a reverse twist or rate cuts by the Fed.

首先,市场预计10年期国债收益率将基本保持在当前水平;第二,市场预计核心交叉货币互换基点将扩大(至负水平),而非是收紧(走正);第三,市场预计Libor-OIS利差将收紧,但只会在边际上小幅收紧;第四,市场预计美联储不会实施逆向扭曲操作(买短卖长)或降息。

If none of this will happen, the curve won’t re-steepen relative to funding costs, primary dealers will continue to struggle with growing Treasury inventories and lean heavily on the o/n GC repo market to fund their inventories, which in turn will push large U.S. banks’ reserve balances to the limits of their flexibility – the Fed would have to end taper prematurely and launch an o/n repo facility.

如果所有这些都不会发生,那么相对于融资成本而言,国债收益率曲线就不会再次变得陡峭,一级交易商将继续艰难应对不断增加的美国国债库存,并严重依赖隔夜的回购市场为其库存(国债)融资,而这反过来又会迫使美国大型银行将准备金余额推至其灵活性的极限;美联储将不得不过早地结束资产负债表的缩减,并启动一项隔夜的回购便利工具。

But the market does not expect that either! Something just does not add up…

但是市场也不这么想!这看起来并不合理。

We expect the Treasury curve to re-steepen relative to hedging costs this year mostly through adjustments in funding markets: through cross-currency bases trading positive, Libor-OIS reaching post-Basel III tights at 10 bps by June, and bill yields trading well below OIS – not as much due to changes in supply, but due to increased demand that will come from positive cross-currency bases.

我们预计今年美国国债的收益率曲线将会相对于外汇对冲成本再陡峭化,而这主要通过融资市场的调整来实现:交叉货币互换基点走正,Libor-OIS利差在六月收窄至10bps,短期国债利率回到OIS下方——不是因为供应问题,而是因为正的交叉货币互换基点带来的增量需求。

These adjustments can of course happen without any help from the Fed. However, if the Fed chooses to aid these adjustment so it can taper for longer, the moves could be even bigger – Libor-OIS could even go negative by June.

这些调整当然可以在没有美联储给予任何帮助的情况下发生。然而,如果美联储选择帮助实现这些调整,使其能够延长其缩表计划,那么这些调整的影响可能会更大——Libor-OIS在6月份甚至可能走负。

Either way, this can be the year when the Fed, after a decade of absence, gets active in money markets again – either as a buyer of bills or a repo lender.

不管怎样,今年可能是美联储在缺席十年之后再次活跃于货币市场的一年。无论是作为短期国债的买家还是回购的融出方。

正文部分

2019年,美国固定收益市场将不得不处理四个令人不安的事实:

The U.S. fixed income market will have to deal with four uncomfortable facts in 2019:

- 美国国债的净供应将增加1万亿美元以上。

- The net supply of U.S. Treasuries will increase by over $1 trillion…

- 美国需要外国投资者购买新供应量中的一部分。但是…

- …and the U.S. needs foreign investors to buy a share of new supply. But…

- 外国的官方买家不再饥渴地购买美国国债……

- …foreign official buyers are no longer voracious buyers of Treasuries, and…

- 外国的私人买家也不太可能在如此高企的外汇对冲成本下购买国债。

- …foreign private buyers are unlikely to buy either due to FX hedging costs.

Foreign investors are still important buyers of Treasuries on the margin, but the switch from foreign official accounts to foreign private accounts as dominant marginal buyers has changed the economics of funding the U.S.’s twin federal and current account deficits.

外国投资者仍然是美国国债的重要买家,但由于当前接力棒已经从外国官方账户转向外国私人账户作为主导性的边际买家,这已经改变了为美国的双重赤字——联邦赤字和经常账户赤字提供资金的经济状况。

Foreign official accounts managed FX pegs and bought Treasuries to manage those pegs

外国官方账户需要管理外汇来维持本币锚定,并购买美国国债不惜一切代价地维持锚定。由于外国官方账户正致力于吸收掉外币投资的外汇风险,因此他们没有对冲他们的美债投资组合,因此也不在乎对冲成本。

Foreign private accounts are a completely different story. Foreign private accounts’ mandates do not allow for much of any FX risk and so hedging costs have a big impact on whether foreign private investors buy U.S. Treasuries or other bonds available globally.

外国私人账户则是一个完全不同的故事。外国私人账户规定不允许承担过多的外汇风险,因此对冲成本对外国私人投资者是否购买美国国债或全球其他债券产生重大影响。

Foreign official accounts were price insensitive – it took no effort to keep them. Foreign private accounts are price sensitive – it will take an effort to keep them.

外国官方账户对价格不敏感,仅需保证持仓即可。外国私人账户则对价格非常敏感,因此需要主动管理来保证持仓。

Just as a global bank’s treasurer constantly calibrates a bank’s funding profile to adjust to changes in the fabric of global funding markets – whether due to money fund reform or corporate tax reform – the U.S. government should now focus more carefully on how to entice price sensitive foreign investors to fund the growing federal deficit on the margin.

正如一家全球银行的司库人员不断调整一家银行的融资状况和结构,以适应全球融资市场结构的变化——无论是货币基金改革还是公司税改革——美国政府现在应该更加谨慎地关注如何吸引价格敏感的外国投资者为日益扩大的联邦赤字融资。

New global funding arrangements suggest that the U.S. Treasury should now tweak its debt management practices and the Fed should consider new factors when setting rates: the optimal mix between bills and coupons at auctions and in the Fed’s SOMA portfolio; the impact that rate hikes have on FX hedging costs and the slope of the Treasury curve relative to the slope of other core government curves globally should be taken into account when thinking about the U.S.’s funding needs – at least to some degree.

新的全球融资条件表明,美国财政部现在应该调整其债务管理的实操,美联储在确定利率时应该考虑新的因素:在美联储的SOMA投资组合中考虑短期国债和中长期国债的结构组成;加息对外汇对冲成本和国债收益率曲线相对于全球其他核心国债收益率曲线产生的影响,应该在考虑美国的融资需求时,在一定程度上纳入对这些影响的考量。

But currently they aren’t, and because they aren’t, flows are changing. Foreign investors and even some U.S. investors have started to leave the Treasury market on the margin!

但目前联储并未如此行事,由于联储的无所作为,资金流动正在产生变化。外国投资者,甚至一些美国投资者已经开始在边际上离开美国国债市场了!

Everything that will transpire in global funding and rates markets in 2019 will come down to how long-term U.S. Treasury yields and FX hedging costs will adjust from here, such that foreign investors up their funding of the U.S.’s growing federal deficits again.

2019年全球融资与利率市场的所有变化都将取决于美国长期国债收益率和外汇对冲成本将如何调整,这样外国投资者就可以再次增加对美国不断增长的联邦赤字的供资。

Depending on whether the adjustment comes from much higher long-term Treasury yields or much lower hedging costs means different things for risk assets and funding markets.

这取决于调整是来自较高的长期国债收益率还是低得多的外汇对冲成本,这对风险资产和融资市场意味着不同的因素。

Sharply higher Treasury yields mean nothing good for equities and credit or the outlook.

如果美国国债收益率走高,这对股票、信贷或经济前景不利。

Sharply lower hedging costs are good for risk assets, but imply a trading regime for funding markets that’s very different from the trading regime of the past four years – one where cross-currency (XCCY) bases are positive, not negative, and where Libor-OIS trades tight, not wide, with a risk that Libor-OIS spreads may even go negative this year.

大幅降低外汇对冲成本对风险资产有利,但意味着融资市场的交易范式与过去四年的交易范式大相径庭——对冲成本——正面交叉货币互换基点将为正,而不再为负,而且Libor-OIS将收窄,而非走高,甚至今年还可能走负。

These changes would of course change banks’ global issuance patterns dramatically – less issuance in dollars and more issuance in yen, euros, sterling and other currencies.

这些变化当然会改变银行的全球发行模式——大幅降低美元发行量,增加日元、欧元、英镑和其他货币的发行量。

They would also re-draw the pattern of global portfolio flows – foreign investors would re-direct their flows toward the U.S. once again, at the expense of German and French government bonds, as well as Australian government bonds and Danish covered bonds.

它们还将重新定义全球投资组合流动的格局;外国投资者将再次将资本流向美国,牺牲德国和法国政府债券以及澳大利亚政府债券和丹麦的担保债券。

Importantly, we do not expect spot FX rates to absorb any of the needed re-alignments, as in a world where flows are increasingly hedged on the margin, adjustments are borne by forward FX rates. That said, similar to how the spot FX rate would have to weaken for a country that needs to attract foreign buyers on the margin, in a world of hedged flows, her forward FX rates would have to weaken – and that’s what positive XCCY bases mean!

重要的是,我们不认为即期外汇汇率能够吸收任何必要的重新调整,因为在这个世界上,资金流动越来越多地在边际上被对冲保护,调整是由远期汇率承担的。尽管如此,对于一个需要在边际吸引外国买家的国家而言,在资金流动的外汇风险被对冲的世界里,正如现货汇率将走弱,远期汇率也必须走弱——这就是交叉货币互换基点走正的含义。

本期《全球货币笔记》有五个部分.

Part one explains why the U.S. used to be a magnet for global portfolio flows until 2017, and why the Fed’s rate hikes changed that – why hikes drove capital away from the U.S., and how this flip-flop in flows changed global funding market dynamics in recent quarters.

第一部分解释了为什么直至2017年为止美国曾是全球投资组合流动的磁石,以及为什么美联储加息改变了这种状况——为什么加息将资本从美国转移,以及近几个季度这种资金流动的变动如何改变了全球融资市场的动态。

Part two explains why traditional measures of Treasury curve inversion are meaningless in a post-Basel III world, and shows that the curve has been inverted for the past six months.

第二部分解释了为何在后巴塞尔协议III世界中,传统的国债收益率曲线倒挂指标毫无意义,并表明过去六个月中这一曲线已经倒挂。

Part three explains why the Treasury curve has to re-steepen and asks whether markets should be left alone to adjust or if Treasury or the Fed should play a role in the process.

第三部分解释了为何国债收益率曲线必须重新陡峭化,并设问市场是否应该独自进行调整,还是由财政部或美联储介入,在这一过程中发挥作用。

Part four explains why it’s consistent with the Fed’s normalization principles to help the curve re-steepen either through a reverse twist or by capping the foreign repo pool.

第四部分解释了为什么它符合美联储的常态化原则,即通过逆向扭曲操作或通过对海外回购池的设置上限来帮助曲线重新变得陡峭。

Part five concludes by explaining why positive cross-currency bases to U.S. dollar Libor are the most likely avenue through which the inversion will be fixed, and how structurally positive cross-currency bases would impact funding and rates market dynamics globally.

第五部分在结尾部分解释了为什么正的交叉货币互换基点以及美元Libor是最有可能反转收益率曲线的途径,以及结构上为正的交叉货币互换基点将如何影响全球融资和利率市场动态。

第一部分:加息和资本流动 Part I – Rate Hikes and Capital Flows

Just two years ago, Japanese banks and life insurers were the main buyers of Treasuries, alongside real money accounts from other negative rate jurisdictions such as Germany, France, the Netherlands, Switzerland and a handful of smaller countries in Scandinavia.

就在两年前,日本银行和寿险企业成为了美国国债的主要买家,此外还有德国、法国、荷兰、瑞士以及北欧的少数几个小国等其他负利率区的实际投资账户。

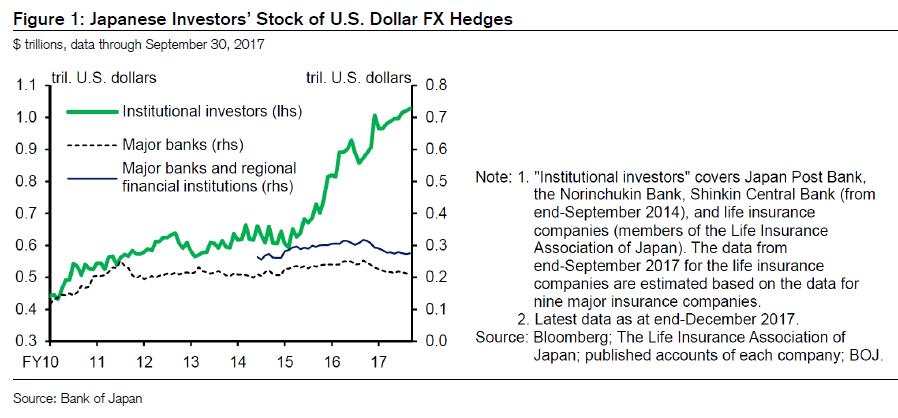

Due to these accounts’ persistent bid for Treasuries, Treasury auctions always went well, and, because their mandate did not allow for FX risks, these accounts bought Treasuries on a hedged basis.2 As such, post-auction funding pressures typically showed up in the FX swap market – three-month cross-currency bases between the U.S. dollar and the yen, euro, Swiss franc and Scandinavian currencies were drifting more negative as the stock of Treasuries held by foreign investors grew and the associated stock of hedges that had to be rolled every three months grew too. For example, Japanese life insurers’ stock of dollar hedges doubled since 2015 and rose to $1 trillion by 2017 (see Figure 1).

由于这些账户对美国国债的持续买入,国债拍卖情况不错。鉴于他们的投资要求中并不允许承担汇率风险(注意:一些账户可能会承担一些外汇风险,但根据经验,大多数外国投资者对大多数外汇风险进行了对冲),这些账户需要在对冲汇率风险的前提下买入美国国债。因此,美债拍卖后的融资压力通常会先出现在外汇互换市场;美元和日元、欧元、瑞郎和北欧数国货币对为期三个月的交叉货币互换基点随着外国投资者持有的美国国债存量增加,以及每三个月必须滚动操作的对冲交易量增加,深陷负值区域。例如,日本寿险公司的美元对冲量自2015年以来翻了一倍,至2017年上升到1万亿美元(见图1)。

Widening cross-currency bases were symptomatic of a global dollar funding market where demand for dollars via FX swaps was greater than the supply of dollars via FX swaps, and the dominant arbitrage trade of the day was banks raising dollars in other funding markets on the margin to bridge that imbalance. These arbitrage trades initially pressured spreads in term unsecured markets, with three-month U.S. dollar Libor moving around the most, but after money fund reform, the funding of arbitrage trades shifted over to repo markets and collateral upgrade swaps became the main channel to source U.S. dollars.

交叉货币互换基点在负值区间不断扩大,是全球美元融资市场的一个标志:即通过外汇互换交易呈现出的对美元的需求大于通过外汇互换交易中美元的供应量,而目前互换市场中主要的套利交易者是银行——银行在其他融资市场上筹集美元,以弥补这种供需失衡。套利交易最先在有期限无担保的融资市场上施压利差,三个月期Libor变动最大,但在货币基金改革后,这些套利交易的资金转移到回购市场,抵押品升级置换成为了获取美元资金的主要渠道。

As cross-currency bases widened, more and more lenders of dollars in money markets were attracted by the spread that lending dollars via FX swaps offered over Treasury bills: several central banks and treasurers at hedge funds and asset managers changed their portfolio guidelines so they could lend dollars via FX swaps to earn this spread.

随着交叉货币互换基点的不断扩大,货币市场上越来越多的美元融出机构被通过外汇互换融出的美元利差(相较于短期国债)所吸引:几家中央银行和对冲基金的司库,以及资产管理公司修改了投资组合准则,以便通过外汇互换的手段贷出美元,赚取利差。

This extra supply of dollars in the FX swap market brought supply more in line with demand, and as the flows became more matched, cross-currency bases stopped widening and started to tighten. Global banks’ and dealers’ need to bridge imbalances in order flows via arbitrage diminished, and with that came less pressure on U.S. dollar Libor and repo rates.

外汇互换市场中这种额外的美元供应使供应更加匹配了美元需求,随着资金流动的更加匹配,交叉货币互换基点在负值区域的扩大停滞了,并开始收缩。全球银行和交易商通过套利交易弥合这种美元失衡的需求逐渐消失,从而缓解了Libor和回购利率的压力。

Figure 2 shows the three-month $/¥ cross-currency basis over time.

图2展示了3个月期的美元/日元交叉货币互换基点随时间的变化。

Like most other cross-currency bases, the three-month $/¥ basis has been grinding more and more negative during 2015 and 2016, just as Japanese real money investors’ stock of hedging needs rose. It then turned sharply less negative coming into 2017, as flows in the FX swap market became more matched and the funding of arbitrage trades post-money fund reform shifted from unsecured markets to the cheaper o/n repo market.

和大多数其他交叉货币互换基点一样,2015年和2016年,3个月美元/日元的基点日益下跌,与此同时,日本的真实货币投资者的对冲需求也有所上升。进入2017年后,随着外汇互换市场的资金流动变得更为匹配,货币基金改革以后的套利交易融资从无担保市场转向了价格更低的隔夜回购市场。

Importantly, the backdrop to widening cross-currency bases – which lasted until 2017 – was a steep Treasury curve. Figure 3 shows that the spread between 10-year notes and three-month bills (henceforth 3s/10s) was a steep 250 basis points (bps) back in 2015 – and with that slope, the Treasury curve was the steepest core government curve globally: 3s10s spreads were 50 bps in Japan and slightly over 100 bps in Germany and France.

重要的是,持续至2017年的交叉货币互换基点不断在负值扩大的一个背景,是陡峭的美国国债收益率曲线。图3显示,10年期国债与3个月期国债(3s/10s)之间的利差较2015年时高出250个基点(bps);随着收益率曲线的走陡,美国国债收益率曲线是全球最陡峭的核心政府债券曲线:3s10s的息差在日本为50个基点,在德国和法国略高于100个基点。

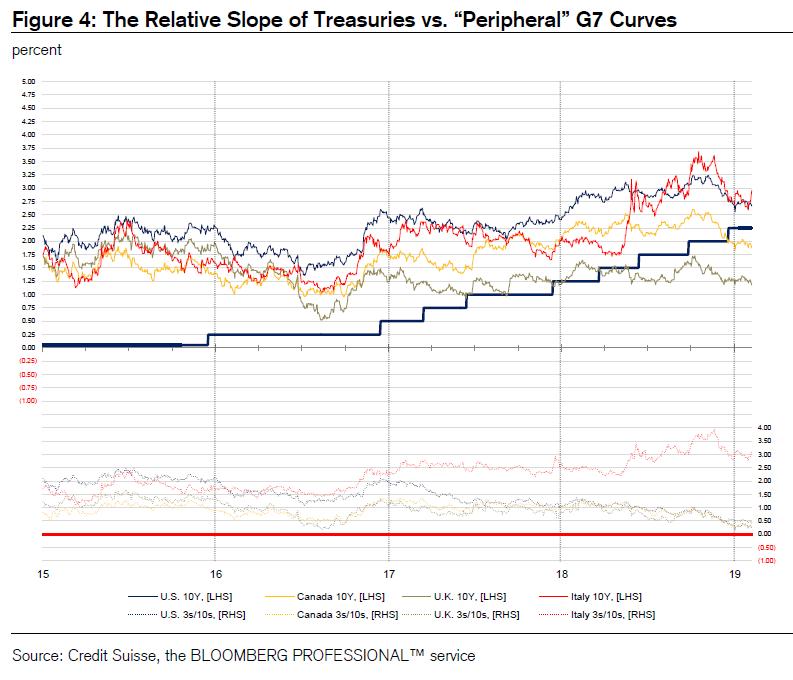

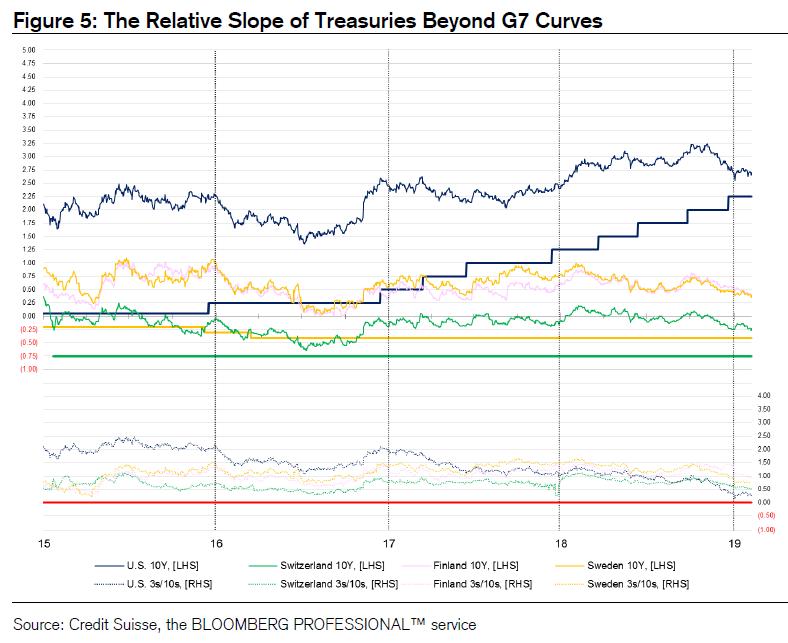

The Treasury curve was steep relative to all other G7 government curves and beyond: Figure 4 shows that spreads in Canada and the U.K. were 50 and 150 bps, respectively, and Figure 5 shows that 3s/10s spreads in Switzerland and Scandinavian countries were about 50 and 150 bps, respectively. The Treasury curve remained the steepest curve globally until the Fed began to accelerate rate hikes in early 2017 (more on this below).

与其他G7政府曲线相比,美国国债曲线更陡峭:图4显示,加拿大和英国的利差分别为50和150bps,图5显示,瑞士和北欧数国的3s/10利差分别为50bp和150bps。直到美联储在2017年初开始加速加息(更多见下文),美国国债曲线仍是全球最高的曲线。

With the Treasury curve 100-200 bps steeper than other core government curves, foreign buyers’ appetite for U.S. Treasuries was understandable and, as a rule of thumb, how negative cross-currency bases traded was a good barometer of how desperate foreign investors were to dump their local currency to buy dollar assets on a hedged basis – the flatter the local curve was, the more eager local investors were to swap the low-yielding local currency for dollars, the more negative the cross-currency basis would go.

这意味着美国国债收益率曲线相比其他核心政府债券的收益率曲线要多出100-200个bps的利差,外国买家对美国国债的胃口因此不难理解,且根据经验判断,交叉货币互换基点在负值区间的程度是一个很好的晴雨表,它可以说明外国投资者是多么迫切地在抛售本币以在对冲的基础上购买美元资产。当地政府债的收益率曲线越是平坦,则当地的投资者越是急于将低收益的本国货币换成美元,交叉货币互换基点就会进一步走负。

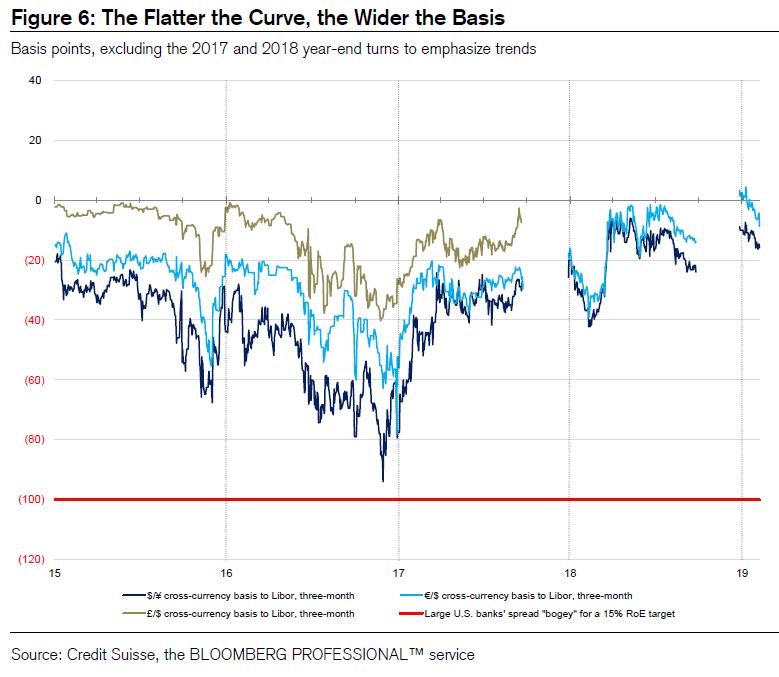

For example, with the Japanese government curve being the flattest core curve in 2015, the $/¥ basis was the most negative cross-currency basis in 2015, meaning that the desire to lend the local currency and buy dollars was strongest in Japan (see Figure 6).

例如,由于2015年日本政府债券的曲线是最为平坦的收益率曲线,2015年美元/日元的交叉货币互换基点在负值区间陷得最深,这意味着融出本国货币且购买美元的意愿在日本最强(见图6)。

German and French curves were a bit steeper than the Japanese government curve, so the €/$ basis was trading at less negative spreads than the $/¥ basis – while Europeans were desperate to get rid of euros, they were relatively less desperate than the Japanese.

德国和法国的收益率曲线则比日本的更陡,因此,欧元/美元的交叉货币互换基点没有美元/日元所处的那么负,欧洲人急于摆脱欧元,但相较之下,他们没有日本人那么迫切了。

The U.K. curve was steeper than either of the above curves, and correspondingly, the £/$ basis was the least negative among the core cross-currency bases back in 2015.

英国的收益率曲线比上述的曲线都陡峭,相应地,在2015年,英镑/美元的交叉货币互换基点在负值区间的水平最浅。

The acceleration of the Fed’s interest rate hikes starting in 2017 changed everything.

从2017年开始,美联储的加速加息改变了一切。

The Fed hiked interest rates eight times for a cumulative 200 bps, which wiped out the global “slope” advantage of the Treasury curve and dramatically increased hedging costs – while in the beginning of 2017, the Treasury curve was still the steepest curve globally, by the end of 2018, it became the flattest curve globally (see Figures 3, 4 and 5 above).

美联储累计加息八次,总计200个基点,抹去了美国国债在全球政府债曲线中的利差优势,并大幅推高了对冲成本;在2017年初,美国国债的收益率曲线仍是全球最陡峭的曲线,而到了2018年底,它却成了全球最平的收益率曲线(见上文的图3、4和5)。

Figure 7 shows the Fed’s impact on FX hedging costs. FX Hedging costs are not uniform across currencies. We use yen-based hedging costs as a benchmark example.

图7展示了美联储对外汇对冲成本的影响。外汇对冲成本在各货币之间并不一致。我们以日元的对冲成本为基准例子。

Money markets are like a cake – sponge, cream, sponge, cream…

货币市场就像一块蛋糕,蛋糕海绵,奶油,蛋糕海绵,奶油。

Hedging costs are the sum of three distinct funding market components: U.S. dollar OIS, the U.S. dollar Libor-OIS spread, and the cross-currency basis to U.S. dollar Libor.4

这里的对冲成本是三个不同的融资市场组成部分的加总:OIS、Libor-OIS以及交叉货币互换基点。

During 2015 and 2016, the “frontier” in funding markets was the cross-currency basis, and, as discussed above, the widening of cross-currency bases routinely bled through to wider Libor-OIS spreads as banks tapped unsecured markets to arbitrage imbalances in the FX swap market. These “add-on” spreads – Libor-OIS and cross-currency bases – on top of U.S. dollar OIS were the dominant component of FX hedging costs back then.

2015年和2016年期间,融资市场的前沿是交叉货币互换基点,如上文所述,随着银行利用无担保市场融入美元以对外汇互换交易市场的美元供需失衡进行套利交易,交叉货币互换基点的扩大施压了Libor-OIS,致使后者也扩大。这些“附加”的利差,立于OIS之上的Libor-OIS以及交叉货币互换基点,是外汇对冲成本的主要组成部分。

During 2017 and 2018, the dynamics changed. OIS started to rise dramatically as the Fed accelerated the pace of rate hikes, and OIS became the dominant component of hedging costs. The add-on spreads had to shrink in a relative sense, as a dramatically flatter Treasury curve didn’t leave much room for foreign investors to pay up for hedges.

在2017和2018年期间,形势发生了变化。随着美联储加快加息步伐,OIS开始大幅攀升,OIS成为对冲成本的主导组成部分。附加的利差不得不对应缩窄,由于美国国债收益率曲线走平——无力给外国投资者支付的对冲成本留下多大空间。

As the Fed’s interest rate hikes piled up the OIS component of hedging costs rose, the U.S. Treasury curve flattened, and, when adding hedging spreads on top of OIS (Libor-OIS and cross-currency bases to Libor), hedging costs practically converged with, and, by the end of 2018, even exceeded the 10-year Treasury yield – Treasury yields, on a hedge-adjusted basis got flat to negative relative to the abysmal local yields that Japanese and European portfolio investors have been trying to escape in the first place!

随着美联储加息推高了OIS这一对冲成本的要素之一,美国国债的收益率曲线亦趋于平坦,且当把对冲利差加到OIS之上以后,对冲成本实际上已经和美债收益率趋同,而且到2018年底时,对冲成本甚至超过了10年期的美国国债收益率;按对冲成本调整后的美国国债收益率相比于日本和欧洲的投资者一直试图逃避的极其糟糕的本地收益率,已为负值!

Once convergence occurred, foreign portfolio investors had no choice but to go down the global rates, credit and liquidity spectrum – they bought IG credit and CLOs in the U.S., and, to diversify away from credit, they started to buy safe, steep and cheaper to hedge core government bond curves elsewhere (for example Germany, France and Spain), but also safe, steep, and cheaper to hedge but relatively illiquid curves on the periphery (for example Australian government bonds and Danish and Swedish covered bonds).

一旦收益率曲线趋同,外国的组合投资者别无选择,而只能选择战略转移,选择承担更高的信用和流动性风险来攫取更高的收益——他们买入美国的投资级信用债以及CLOs。此外,为了多元化其信用风险,他们开始在别处买入安全的、陡峭的、对冲起来比较便宜的核心政府债券(曲线)。比如德国、法国和西班牙的国债,同时那些安全、陡峭的、对冲起来便宜、但流动性不怎么好的外围国家债券也作为了选项——比如澳大利亚政府债券以及丹麦、瑞典的担保债券。

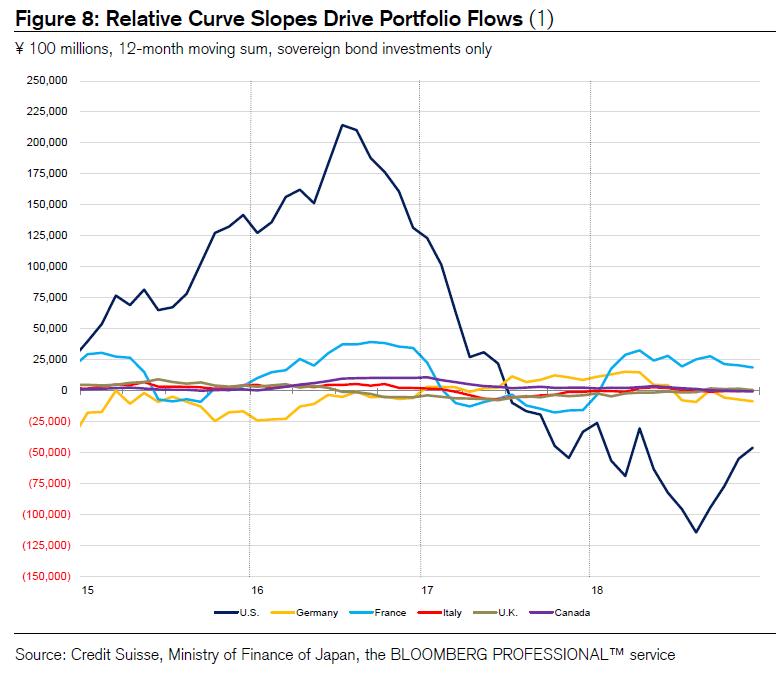

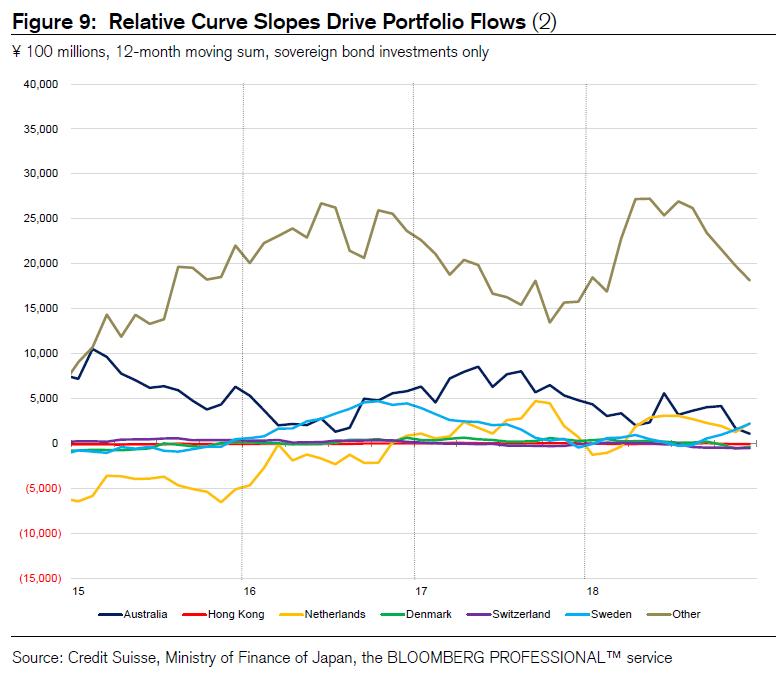

Sticking with Japanese portfolio investors as our benchmark example, Figures 8 and 9 shows the dramatic change in Japanese portfolio flows since the Fed started to hike rates. The net impact of these changing flows has been an inflexion point in the global demand for dollars in the FX swap market: less demand, not more, relative to 2015 and 2016.

图8和图9展示了自美联储开始加息以来日本投资组合流动的急剧变化。这些流动变化的净影响成为了外汇互换市场美元全球需求的一个拐点:与2015年和2016年相比,需求减少了,而非增加了。

Thus, just as the financial system was getting more efficient at providing dollars to the FX swap market to feed the hedging needs of foreign investors, the acceleration of hikes from 2017 onwards started to sap foreign portfolio investors’ demand for dollar assets and associated dollar hedging needs. This explains why – apart from year-end turns – the $/¥ and €/$ bases have been steadily grinding tighter during the Fed’s hiking cycle.

因此,正如金融系统在向外汇互换市场提供美元以满足外国投资者对冲需求方面变得越来越有效率一样,从2017年起,加速加息开始削弱外国投资者的美元资产需求和相应的美元对冲需求。这就解释了为什么除了年终(因为监管要求引致)的突然反转走负以外,在美联储的加息周期中,交叉货币互换基点一直在稳步收紧。

One lesson from our analysis so far is that the relative slope of core curves matters and that hedging costs matter too. Rate hikes can push the U.S. rates market in a corner if they flatten the curve and if hedging costs deter, rather than attract foreign capital flows!

到目前为止,我们的分析所得到的一个教训是,核心(资产收益率)曲线的相对斜率很重要,对冲成本也很重要。如果利率的上升拉平了收益率曲线,如果对冲成本吓阻而非吸引外国资本的流动,利率上升会将美国利率市场逼到角落!

One “dirty” downside of the Fed’s current hiking cycle to date is that hikes have been pushing foreign portfolio flows away from the U.S. on the margin – not attracting them.

到目前为止,美联储的加息周期有一大负面效应,即导致外国投资组合在边际上从美国流出,而非吸引了外资。

The Treasury curve going from the steepest government curve to the flattest globally had a drastic impact on the demand for Treasuries at auction and how funding markets trade.

从全球最陡的国债收益率曲线到最平,都对美国国债拍卖市场的需求以及融资市场交易方式产生了重大影响。

In a remarkable contrast to two years ago, foreign buyers are routinely absent from Treasury auctions, and primary dealers are routinely stuck with Treasuries after auction, which take considerable time and effort to work through and distribute to end-investors.

与两年前形成鲜明对比的是,美债拍卖上时长见不着外国买家的身影,而一级交易商则在拍卖后被塞了一大堆国债,此后还得花时间和精力来分发给终端投资者。

Importantly, just as foreign investors are staging a buyer’s strike, the size of auctions is getting bigger for two reasons: growing federal deficits and the Fed’s balance sheet taper.

重要的是,正当外国投资者正在上演买方*工罢**时,国债拍卖的规模却正在扩大,原因有二:联邦赤字不断增加,美联储的资产负债表逐渐缩小。

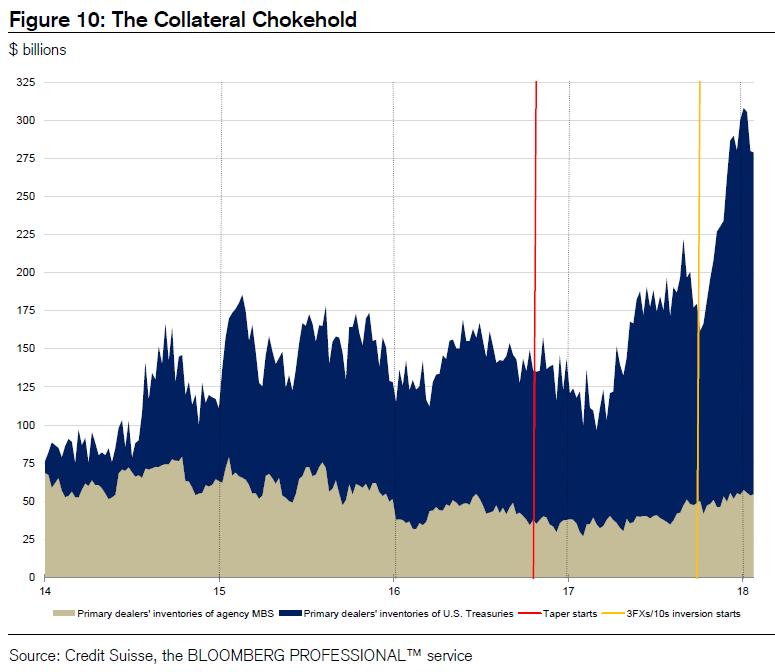

In 2018, primary dealers’ inventories of Treasuries expanded by about $150 billion – which was $150 billion that the rest of the world used to buy, but currently couldn’t due to hedging costs. Some of these Treasuries came from net new Treasury issuance and some from balance sheet taper. When we include the taper of the agency MBS portfolio, there is an additional $50 billion increase in dealer inventories from taper (see Figure 10).

2018年,一级交易商的国债库存增加了约1500亿美元,这是本由世界其他国家买走,但目前由于对冲成本的问题,外国的买家无法消化掉这些国债。其中一些国债来自新发行的国债,还有一些则来自美联储资产负债表逐步缩减。如果将投资组合中的机构MBS缩减涵盖在内,一级交易商因联储缩表导致的库存量增加还会有额外500亿美元(见图10)。

Thus, primary dealers’ inventories of Treasuries and agency MBS increased by roughly $200 billion last year, because foreign buyers, in sharp contrast to the recent past, can no longer buy these assets on a hedged basis. Primary dealers getting routinely stuck with new supply of Treasuries and agency MBS in turn changed funding market dynamics.

因此,一级交易商的美国国债和MBS库存量在去年大约增加了2000亿美元,这与过去几年的情况形成了反差,外国买家无法再以外汇对冲方式的购买这些资产。一级交易商总是被新的美国国债和机构MBS供应所困,而这反过来改变了融资市场的动态。

Two years ago, when foreign private buyers took down the bulk of Treasuries at auction, funding pressures showed up in the FX swap markets and related arbitrage activities as foreign buyers had to hedge their Treasuries back to yen, euro and other currencies.

两年前,当外国私人买家在国债拍卖上认购大量的美国国债时,外汇掉期市场和相关套利活动出现了融资压力,因为外国买家不得不对冲美国国债的汇率风险,使其回归日元、欧元和其他货币计价。

Today, when primary dealers get routinely stuck with the bulk of Treasuries after auction, funding pressures show up in the repo market as dealers scramble to fund inventories.

如今,当一级交易商在美债拍卖后不可避免地被塞了一大堆美国国债时,在回购市场出现了融资压力,交易商争相为这些资产库存进行融资。

This pendulum swing from Treasuries ending up mostly with end-investors funding at the three-month point in the FX swap market to Treasuries getting stuck in inventory with dealers having to fund them in the repo market is what’s behind the shift in funding market dynamics in recent quarters. While it may seem odd that cross-currency bases are “asleep” while the repo market is trading stressed occasionally, that’s no more odd than the Northern hemisphere braving a polar vortex while Australia is fighting serious wildfires.

国债的钟摆引发的传导链条(终端投资者胃口变小→货币互换需求下降→国债充斥于交易商的库存内→交易商不得不在回购市场为其库存融资)是近几个季度融资市场动态变化的背后原因。尽管当回购市场偶尔受到压力时交叉货币互换基点的“冬眠”似乎有些奇怪,但这并不比北半球面对极地漩涡和在澳大利亚与严重的野火作斗争更奇怪。

What climate change is to weather patterns, curve slopes are to funding patterns… The arbitrage trades banks are engaged in are also different from the previous regime.

气候变化对天气模式的影响类似曲线斜率对融资模式的影响;银行所从事的套利交易也与之前的范式不同。

Two years ago, global banks were busy deploying reserves in their HQLA portfolios to harvest deeply negative cross-currency bases, or, alternatively they tapped unsecured and secured markets to raise dollars to lend in the FX swap market on the margin (see here).

两年前,全球银行正忙着在其HQLA投资组合中配置准备金,以攫取深陷负值的交叉货币互换基点的收益,或者通过利用无担保和有担保市场筹集资金,以便在外汇互换市场上融出美元。

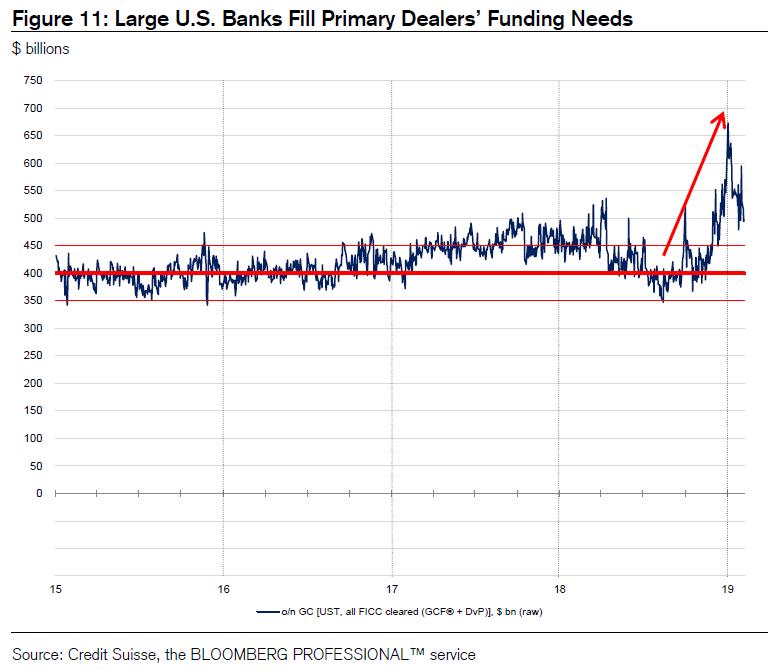

Today, global banks are busy deploying reserves from their HQLA portfolios to harvest o/n GC repo rates trading above the IOR rate as dealers scramble to fund their inventories.

如今,随着一级交易商争相为其资产库存融资,全球银行正忙着从其HQLA组合中调配准备金,以收获高于美联储存款准备金利率的隔夜一般抵押品回购利率。

Figure 11 shows a massive increase in large banks lending their excess reserves in the o/n GC repo market during the final months of 2018, which is precisely when whatever residual steepness there was left in the Treasury curve suddenly collapsed, hedging costs eclipsed the entire Treasury curve, the foreign marginal bid completely vanished, and dealers’ inventories of Treasuries started to pile up as dealers became the marginal buyer.

图11显示,在2018的最后几个月,大银行在隔夜一般抵押品回购市场中融出的超额准备金呈现大幅上升,巧合的时,此时美债收益率曲线仅剩的陡峭度瞬间崩塌,对冲成本蚕食掉了整个国债收益率曲线,外国的边际买单完全消失了,而交易商的美债库存则开始堆积——交易商成为了边际上的美债买家。

Figure 11 is the conceptual equivalent of Figure 1 – both show surging funding needs, or more precisely, the surging funding needs of the marginal buyer of U.S. Treasuries.

图11与图1在概念上是等同的,两张图都显示了激增的资金需求,或者更准确地说,是美国国债边际买家激增的资金需求。

Two years ago, the marginal buyer was a foreign hedged buyer whose funding needs pressured the three-month point in the FX swap market on the margin (see Figure 12).

两年前,这个边际买家是一个外汇对冲的外国买家,由于其资金需求,外汇互换市场的3个月远期节点在边际上受到了压力(见图12)。

Today, the marginal buyer is a primary dealer whose funding needs pressure the o/n point in the GC repo market on the margin. Figures 11 and 12 explain everything you need to know to understand why repo is trading stressed while cross-currency bases are “asleep”.

如今,边际买家是一级交易商,其融资需求对隔夜一般抵押品回购市场在边际上造成了压力。图11和图12解释了所有你需要了解的情况,以了解为何在交叉货币互换基点处于“休眠”状态时回购交易则处于紧张状态。

In two years, the U.S. has gone from having the steepest government curve to having the flattest government curve; from attracting foreign portfolio flows to deflecting foreign flows; from the dollar being scarce in global funding markets, to the world swimming in dollars; from end-investors buying Treasuries at auction, to Treasuries getting stuck with dealers.

两年来,美债从最陡峭转变为最平坦的政府债收益率曲线;从吸引外国的组合流入转变为外资撤离;从美元在全球融资市场稀缺,到世界被泛滥的美元流动性洗礼;从最终投资者在财政部拍卖时购入美国国债,到美国国债落入交易商之手。

We went from a system that “flew”, to a system that stalled…

我们从一个飞行系统转变为一个停滞的系统。

第二部分:倒挂指标 Part II – Measures of Inversion

Planes stall when their nose is pulled too high – i.e., when the body of the plane “inverts”.

当飞机的鼻子被拉得太高时(比如机身反转时),飞机就会失速。

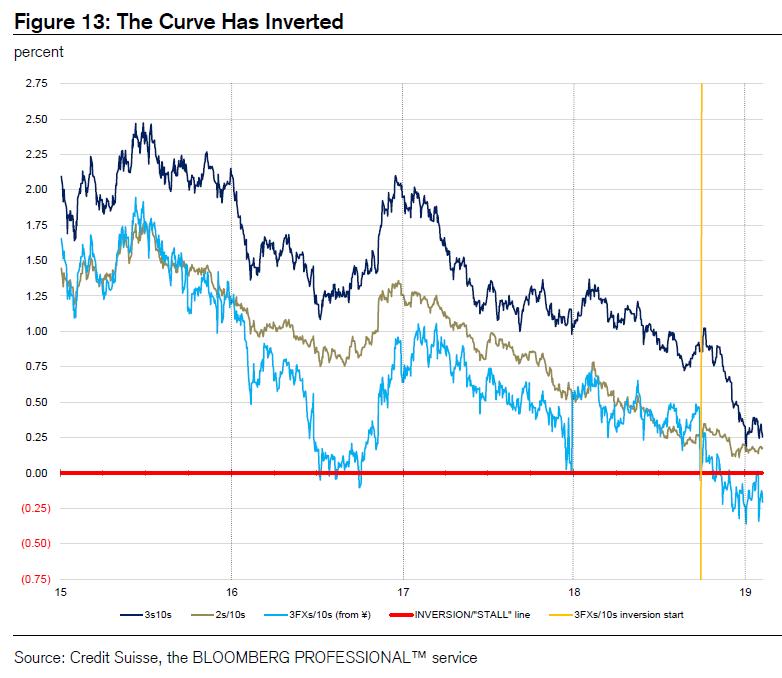

We haven’t mentioned inversion in the prior section explicitly, but a key point we’ve made implicitly is that the Treasury curve outright inverted during the final months of 2018 – relative to foreign investors’ FX hedging costs. So much for the market’s obsession of waiting for when the curve will invert, and what that inversion will mean for the outlook.

我们在前一节中没有明确提到倒挂,但我们隐晦地指出,在2018年的最后几个月,美国国债收益率曲线直接倒挂了——相比于海外投资者的外汇对冲成本倒挂。市场对于等待收益率曲线何时倒转的痴迷,以及倒挂对经济前景的意义,都就此终结了。

A far more important question is what inversions mean for the flow of Treasury collateral – do auctions go well or do they “stall”. All else follows from there, as we will explain below.

一个更重要的问题是,倒挂对于美债抵押品的流动意味着什么?拍卖是否进展顺利还是出现了“失速”?这一切都从那里开始,我们将在下文论述。

Historically, inversions were measured by tracking the 3s/10s spread, but recently the market started to track inversions using the 2s/10s spread instead – the spread between 2-year and 10-year Treasuries. But this measure is flawed and misleading, in our view.

从历史上看,倒挂是通过追踪3s/10s的利差来衡量的,但最近,市场开始采用2s/10s的利差来追踪倒挂情况——2年期美国国债和10年期美国国债的利差水平。但是,我们认为,这项指标存在缺陷和误导性。

Historically, tracking inversions using 3s/10s had meaning to them because funding rates – Libor, repo and hedging costs – all traded at fairly tight spreads to three-month bills, and so the three-month bill yield was a reasonable proxy for investors’ funding costs. In a post-Basel III financial order, however, such comparisons are largely meaningless, as effective funding costs can at times be much higher than bill yields, as shown above.

从历史上看,使用3s/10s来跟踪倒挂情况对他们来说意义重大,因为融资利率——Libor,回购利率以及对冲成本——相比于三个月美国短期国债的利差水平都很紧,因此对于投资者的融资成本而言,三个月短期国债的收益率是个很好的代理指标。然而,在后《巴塞尔协议III》的金融体系中,这种比较基本上毫无意义,因为如上文所示,有效的融资成本有时可能远高于美国短期国债的收益率。

But switching from 3s/10s to 2s/10s is not a reasonable solution as no one funds at the 2-year Treasury yield, and 2s/10s says nothing about foreign demand for Treasuries, and as we’ve explained in the previous section, given that the U.S. is a borrower country, flows from foreign investors are imperative for the U.S. to fund its growing twin deficits.

但是,从3s/10s改为2s/10s并不是一个合理的解决方案,因为没人在2年期美国国债收益率的水平融资,2s/10s并不能说明外国对美国国债的需求,正如我们在前一节所解释的那样,鉴于美国是一个借款国,外国投资者的资金流动对美国不断增长的双重赤字是必不可少的。

More precisely, with foreign official demand on the wane, foreign private demand is now an important part of funding the deficits, and foreign private demand comes only on an FX hedged basis, and only if yields are right relative to FX hedging costs on the margin!

更准确地说,随着外国官方需求的减少,外国的私人需求现在是美国赤字融资的重要组成部分,外国私人需求只能在外汇风险得以被对冲的基础上产生,而且只有在美国国债收益率与外汇对冲成本相比在边际上存在优势的情况下才会产生。

Inversions – defined as three-month hedging costs trading above the 10-year yields (henceforth “3FXs/10s”) – imply that hedging costs and yields are grossly misaligned. Figure 13 shows the traditional, the new and our preferred measures of inversion, that is, 3s/10s, 2s/10s and 3FXs/10s (based on both yen and euro) spreads, respectively: while the traditional and new spread measures suggest that inversion has yet to occur, our measures show that we’ve been living with a curve inversion for the past four months!

倒挂——应当被定义为高于10年期美国国债收益率的3个月外汇对冲成本(3FXs/10s),这意味着对冲成本和美债收益率严重背离。图13展示了传统的、新的以及我们所偏好的倒挂指标,即3s/10s、2s/10s和3FXs/10s(以日元和欧元为基础):尽管传统的和新的倒挂指标表明,倒挂现象尚未发生,但我们的指标表明,在过去四个月里,我们处于曲线倒挂的环境中!

The rest of this section describes how misaligned U.S. funding and capital markets currently are, and how unattractive the Treasury curve is relative to other curves globally.

本节的其余部分描述了美国目前的融资和资本市场失调,以及国债收益率曲线与全球其他收益率曲线相比是多么不吸引人。

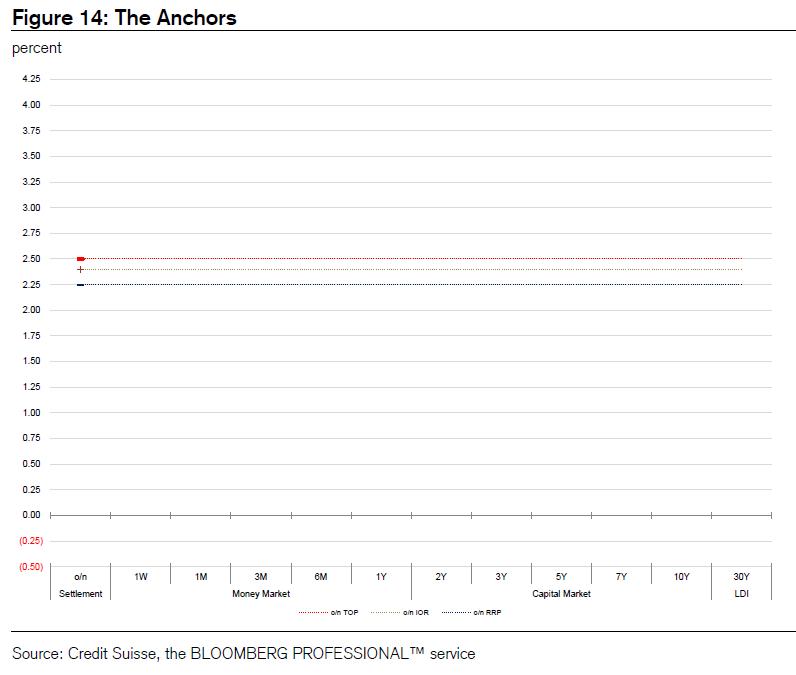

Figure 14 shows the anchors of U.S. rates markets – the o/n RRP rate, the IOR rate and the top of the Fed’s target range for the overnight rates complex. These anchors have gone from practically zero at the end of 2016 to as high as 2.25% - 2.50% as of today.

图14显示了美国利率市场基准利率——即ONRRP利率(隔夜逆回购利率)、IOR利率(存款准备金利率),以及联储政策隔夜利率的目标区间上沿。利率从2016年底的0利率水平上升到今天的2.25%-2.50%。

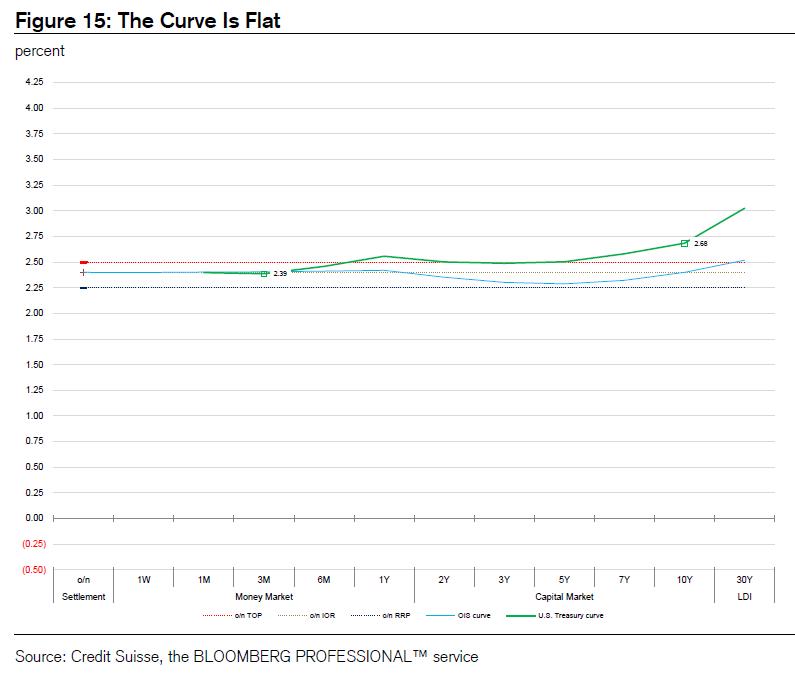

Figure 15 shows the OIS curve and the Treasury curve. Both curves are extremely flat – as discussed above, the Treasury curve is currently the flattest core curve globally!6

图15展示了OIS曲线和国债曲线。这两条曲线都极其平坦——如上所述,目前在全球范围内美国国债的收益率曲线是最平坦的!

Figure 16 shows money market (that is, funding) curves relative to capital market curves: the GC repo curve and the U.S. dollar Libor curve. The position of these curves relative to the Treasury curve actually makes traditional measures of curve flatness look even worse.

图16显示了货币市场(即融资市场)曲线相对于资本市场曲线:一般抵押品回购曲线和美元Libor曲线。这些曲线相对于美国国债收益率曲线的位置,实际上使得传统的曲线平坦程度的测量指标看起来更糟糕。

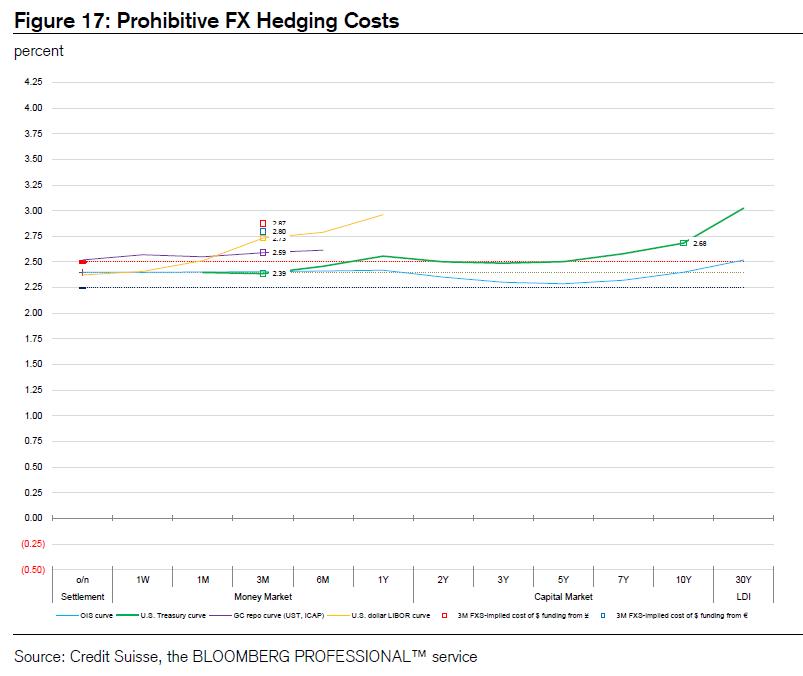

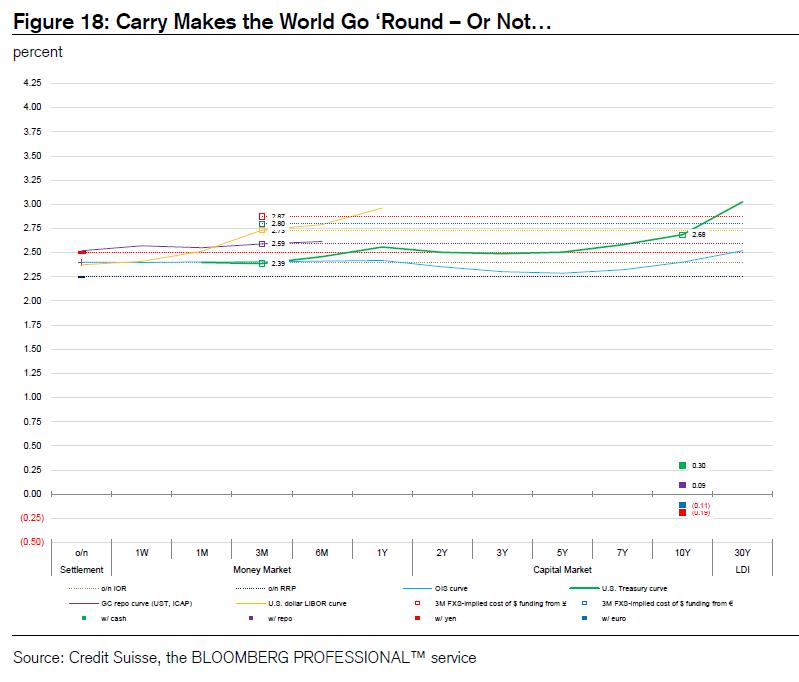

Figure 17 brings three-month FX hedging costs into the picture.

图17将3个月期的外汇对冲成本纳入了图表。

The red square shows the hedging cost of investors that swaps yen for U.S. dollars, and the blue square shows the hedging cost of investors that swaps euros for U.S. dollars.

这个红方框展示了将日元置换成美元的投资者的对冲成本,而蓝方框则展示了将欧元置换成美元的投资者的对冲成本。

Hedging costs are the highest for yen-based portfolio investors: at close to 3.0%, yen-based hedging costs are above the 10-year yield – the inversion we’ve noted above. Hedging costs are somewhat lower for euro-based portfolio investors, but only marginally.

对冲成本对日元投资组合的投资者来说是最高的:基于日元的外汇对冲成本接近3%,高于10年期美债的收益率——这就是我们所说的倒挂。而对于欧元的投资组合而言,对冲成本较低,但只是在边际上更低。

Figure 18 draws a straight line at the current levels of three month GC repo, unsecured and yen and euro-based hedging costs across the entire term structure to show where funding costs are relative to the 10-year yield. In the lower right area, we show spreads earned by various investors that buy the 10-year and fund at various three-month points:

图18是当前的三个月一般抵押品回购利率、无担保融资利率以及日元和欧元的对冲成本(完整的期限结构),以展示融资成本相对于10年期美债收益率的情况。在右下区域,我们展示了不同的投资者以三个月期(不同的)融资成本购买10年期美债可以获得的利差:

for an asset manager forgoing the three-month bill yield the spread is 35 bps;

对于资产管理公司而言,放弃三个月期的短期国债收益率,利差为35个基点;

for a bank funding at the three-month Libor rate, the spread is nil;

对于以三个月期Libor融资的银行而言,利差为零;

for an investor hedging euros for dollars for three months, the spread is -5 bps;

对于欧元对冲(置换为美元)的投资者而言,利差为-5个基点;

for an investor hedging yen for dollars for three months, the spread is -15 bps.

对于日元对冲的投资者来说,利差是-15个基点。

These spreads show very clearly how painfully flat the Treasury curve currently is, why no one will buy Treasuries unless the curve steepens relative to funding costs, why Treasury auctions are going so bad, and why dealers get routinely stuck with Treasuries.

这些利差水平非常清楚地表明,目前的美国国债收益率曲线是多么平坦,为什么除非这一收益率曲线相对于融资成本急剧上升,否则没人会购买美国国债,为什么国债的拍卖情况如此糟糕,以及为什么交易商总是被塞了一大堆美国国债。

First, at 35 bps, asset managers are better off buying three-month CD and CP as these instruments earn the same spread over three-month bills as the 10-year Treasury note – choosing the same amount of spread for a lot less duration risk is an absolute no-brainer.

首先,在35个基点的利差水平上,资产管理公司购买3个月期的存单(CD)和商业票据(CP)会比较好,因为这些工具可以赚到的利差和美债的3s10s利差水平类似;同样数额的利差,还可以降低期限风险这一点优势很好理解。

Second, with three-month U.S. dollar Libor trading in line with the 10-year Treasury yield, its uneconomic for banks to buy Treasuries at any maturity as HQLA – this is the flipside of the case of asset managers, who currently prefer to fund banks over the government.

其次,由于3个月期的Libor与十年期的美国国债收益率不相上下,银行购买任何期限的美国国债作为高质量的流动性资产看上去都不太经济。这也对应了我们在上面提到的资管公司的案例,相比于国债,他们宁可把资金投入到银行(的负债中)。

Third, at hedge-adjusted yields of -15 bps and -5 bps, neither yen-based, nor euro-based portfolio investors have any incentive to buy Treasuries as they earn better yields at home.

第三,利差在对冲调整后为-15bps和-5bps时,无论是基于日元的,还是基于欧元的投资组合管理者,都没有任何动力去购买美国国债,因为它们本国的收益率更高。

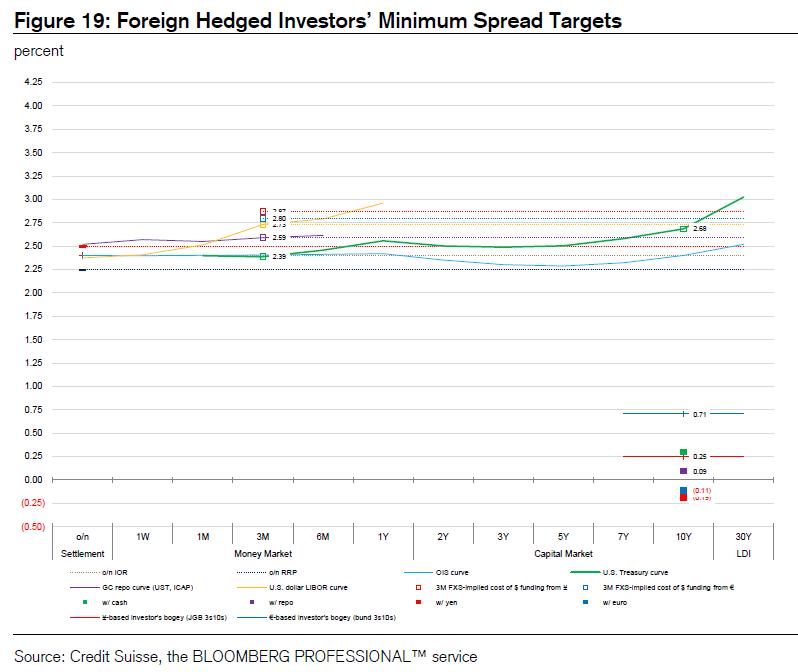

Figure 19 puts the hedge-adjusted yields of euro and yen-based investors into context.

图19将欧元和日元投资者按对冲成本调整的收益率纳入了进来。

The red line shows that by staying home in Japan, a yen-based portfolio investor buying 10-year Japanese government bonds makes 25 bps over three month Japanese bills – a Japanese investor would not buy Treasuries unless FX hedged spreads exceed 25 bps.

红线显示,把资金驻留在日本本土时,以日元投资的证券投资者购买10年期日本政府债券,相比于三个月的短期日本国债有25个基点的利差,除非外汇对冲以后投资于美债的利差超过25个基点,否则日本投资者不会购买美国国债。

The blue line shows that by staying home, a euro-based portfolio investor buying the 10-year German bund can make 75 bps over three-month German government bills – this investor would not buy Treasuries unless FX hedged spreads exceed 75 bps. Using the French curve as the basis, hedged yields would have to exceed 100 bps (not shown).

蓝线显示,把资金驻留在欧元区本土时,以欧元投资的证券组合投资者购买德国10年期国债,相比于三个月的短期德债有75个基点的利差;除非外汇对冲以后投资于美债的利差超过75个基点,否则欧元区的投资者不会购买美国国债。如果我们以法国国债的收益率曲线为基准,对冲以后投资于美债的利差必须超过100个基点(未显示在图中)。

But importantly, similar spread targets apply to large U.S. banks and asset managers.

但重要的是,类似的利差目标适用于美国的大型银行和资产管理公司。

Given the flatness of the Treasury curve, large U.S. banks and large asset managers’ unconstrained, absolute return funds with global mandates are now doing precisely what Japanese investors have been doing for the past five years – lending the local currency, in this case the U.S. dollar, and buying European government bonds on a hedged basis!

鉴于美国国债的收益率曲线如此平坦,美国大型银行和大型资产管理公司——不受约束且具有全球授权的绝对收益基金——现在正像过去5年的日本投资者所做的那样——融出本币美元,并以对冲的方式购买欧洲政府债券。

The spread over 10-year Treasuries earned by U.S. banks and asset managers by swapping dollars for euros at the three month point and then buying 10-year bunds or French government bonds is 100 bps and 125 bps, respectively, which are 25 bps higher than the minimum spread target of euro-based investors to buy Treasuries on the margin.

美国的银行和资产管理公司以三个月期的美元置换成欧元,随后购买10年期德国国债或法国国债而赚取的相比于10年期美国国债的利差水平,分别为100个基点和125个基点,比欧元投资者在边际上(通过对冲手段)购买美国国债的最小利差目标高出25个基点。

These examples make it clear that given the $1 trillion in net Treasury supply this year, prohibitively high hedging costs, and more attractive core government curves elsewhere, the Treasury curve must steepen by at least 100 bps relative to funding costs for foreign and some types of domestic accounts to start buying Treasuries on the margin again.

这些例子表明,鉴于今年美国国债的净供应额达到1万亿美元,且对冲成本高得令人望而却步,以及其他地方更具吸引力的核心政府债券收益率曲线,美国国债的收益率曲线必须相对于外国账户和一些国内账户的融资成本急剧增加至少100个基点,才能重新在边际上吸引到买家。

If it doesn’t, auctions could continue to go bad, dealers inventories will continue to grow, and the Fed could soon have to end taper – which we believe it just does not want to do.

如果曲线难以陡峭化,拍卖情况可能继续恶化,交易商的库存将继续增加,美联储可能很快会结束缩表,而我们认为联储不想这么快结束缩表。

(未完待续)

声明:本文仅代表作者个人观点,不代表智堡立场;文中图片来源于网络,如有侵权烦请联系我们,我们将在确认后第一时间删除,谢谢!

初见智堡,欢迎关注我们的公众号(zhi666bao);喜欢我们的文章,敬请帮助我们分享传播。喜欢智堡,欢迎使用我们的APP、小程序。常驻智堡,请订阅智堡精选,支持智堡的通天之旅。