What Caused the New York vs. London Gold Price Spread and Why it Persists

by Jan Nieuwenhuijs

The spread between the New York futures and London spot gold price was initially caused by logistics and manufacturing constraints, and likely persists because of credit restrictions.

纽约黄金期货合约的报价和伦敦现货金价之间的价差最初与物流和生产环节的制约有关,并有可能因融资不畅而持续下去。

If you read into the economics of commodities, much of it is about geography. The Corona crisis and its effects on global aviation has disrupted large shipments of gold, and created price discrepancies geographically. Normally, bullion is transported in passenger planes, but as those have stopped flying, there is more friction in bullion logistics. Partially, this created the spread between the futures gold price in New York and the London spot price. In my view, the spread persists because arbitragers don’t have enough access to funding, and demand in New York remains elevated.

如果对大宗商品的定价机理有一些了解,就会知道大宗商品的定价在很大程度上会受到地理因素的影响。新冠危机的爆发及对全球航空运输的影响严重干扰了黄金的大规模运输,并导致全球各地的金价走势不同步。金块一般是用客机运输的,但当航空客运因故终止之时,金块的物流就会出问题,这是纽约黄金期货合约的报价和伦敦现货金价之间出现价差的原因之一。我认为这个价差会持续一段时间,因为从事套利交易的机构或人士得不到足够的融资支持,同时纽约对黄金的需求仍居高不下。

How it Started

纽约金价和伦敦金价的走势分化是怎么出现的?

On March 14, 2020, President Trump started curbing passenger flights between Europe and the US. Including those from Switzerland, where the four largest gold refineries of the world are located. This didn’t happen in isolation. Passenger flights all over the world were being curbed. One of the most important airports in London—home of the largest gold spot market by trading volume—is Heathrow. Since March 10, 2020, arrivals at Heathrow started declining from 600 flights per day, to 250 two weeks later.

特朗普大统领在2020年3月14日下令开始削减欧洲和美国之间的旅客航班,其中包括来自瑞士的航班,而瑞士是全球四家最大的黄金精炼企业所在地。受影响的不仅限于瑞士,全球各地的航班都被限制前往美国,一个非常重要的全球性机场——希思罗机场位于伦敦,而伦敦的黄金现货交易量位居全球第一。自2020年3月10日起到达希思罗机场的航班数量从每日600班下降至两周后的250班。

On March 23, 2020, three refineries in Switzerland where temporarily shut down due to the coronavirus. Reuters reported:

2020年3月23日,瑞士有三家黄金精炼厂因新冠疫情而关门歇业。路透社报道如下:

Three of the world’s largest gold refineries said on Monday they had suspended production in Switzerland for at least a week after local authorities ordered the closure of non-essential industry to curtail the spread of the coronavirus.全球最大的黄金精炼厂中的三家在周一宣布其在瑞士的黄金生产将被暂停至少一周,因瑞士当局要求关停非急需的行业运营以遏制新冠疫情的扩散。 The refineries - Valcambi, Argor-Heraeus and PAMP - are in the Swiss canton of Ticino bordering Italy, where the virus has killed more than 5,000 people in Europe’s worst outbreak.这三家黄金精炼厂:Valcambi, Argor-Heraeus和PAMP位于瑞士临近意大利的提契诺州,而意大利的疫情是欧洲最严重的,病亡人数已超过5,000。

Normally, airlines transporting gold and refineries manufacturing small bars from big bars, or vice versa, keep the price of gold products across the globe in sync. If supply and demand for gold in one region is out of whack relative to another, arbitragers step in (buy low, sell high). But with planes not flying and refinery capacity crippled, everything changed.

按照惯例,航空公司负责实物黄金的运输,黄金精炼厂的作用则是将大的金块切割成小块,或反过来讲小块黄金重铸成大块,这些操作确保了全球各地的黄金价格保持一致。如果某个地区的黄金供求关系与其他地区相比出现异常,套利机构会进场低买高卖。但如果飞机停航外加黄金精炼厂停工,一切就会大不一样。

Making delivery at the New York futures market, the COMEX, wasn’t that simple anymore. As we all know, shorts and longs on the COMEX are mostly naked. They either don’t have the metal to make delivery (shorts), or don’t have the money to take delivery (longs). In normal circumstances this isn’t a problem because neither shorts or longs are interested in physical delivery. They trade futures to hedge themselves or speculate. However, when sourcing small bars from Switzerland—only 100-ounce and kilobars are eligible for delivery of the most commonly traded COMEX futures contract—became “more difficult,” the shorts became nervous.

在此情况下,在纽约黄金期货交易所COMEX进行黄金的实物交割将不再像以前那么顺畅了。众所周知,纽约黄金期货交易所COMEX的黄金期货合约的多空双方大多手里没有任何现货。空头拿不出实物黄金交割给多头,多头也拿不出那么多现金头寸吃进实物黄金。正常的情况下这都不是事,因为黄金期货合约的多空双方都无意交割实物黄金,他们买卖黄金期货合约的目的是对冲自身持仓的风险或投机获利。但是,如果从瑞士获得小分量的金块变得“非常困难”,只有100盎司一块或一公斤一块的金块才符合纽约黄金期货交易所COMEX黄金期货合约的交割标准,黄金期货合约的空方会开始坐卧不安。

Likely, after the refineries closed, shorts wanted to close their positions as soon as possible to avoid making delivery. Closing a short position is done by buying long futures to offset one’s position. These trades were driving up the price in New York, and the spread was born.

同理,当黄金精炼厂被迫关门,黄金期货合约的空方想尽快平掉空头仓位以避免进入实物交割程序,买进期货合约就可以平掉空头仓位。正是这种操作拉高了纽约黄金期货合约的报价,并导致与伦敦现货金价之间出现价差。

The white line is London spot, blue is New York futures. Normally, the spread is close to $1.5 dollars ; on March 25, 2020, the spread was $60 dollarsper troy ounce.

上图中白线为伦敦现货金价,蓝线为纽约黄金期货合约的报价。这两个报价之间的价差在正常情况下为1.5美元/盎司,但2020年3月25日该价差增至60美元/盎司。

Usually, such a spread is closed by arbitragers (often banks). They buy spot (London) and sell futures (New York) until the gap is closed. If necessary, these arbitragers hold their position until maturity of the futures contracts, and make delivery to lock in their profit. But because flights were cancelled and refineries were shut down, the “arb” was risky and the spread didn’t close.

正常情况下,这么大的价差会被套利机构(主要以商业银行为主)抹平。套利机构会在伦敦市场买入黄金现货,然后在纽约卖出黄金期货合约,直到这两者之间的价差被抹平。如果有必要的话,套利者会持仓黄金现货的头寸,直到黄金期货合约到期后进行实物交割,这样就能锁定套利收益。但由于航班被取消以及黄金精炼厂关张,这种套利操作的风险变得很高,伦敦黄金期货和纽约黄金现货之间的价差无法抹平。

So you mean the gold futures market “freaks out” exactly at the moment when refineries are shut down and airplanes stop flying? What coincidence. Maybe this market had something to with physical supply and demand after all ;-) — Jan Nieuwenhuijs (@JanGold_) March 26, 2020

Bullion Banks Losing Money Through EFPs

金砖银行在黄金期货转现货的交易中亏钱

Bullion banks often have a long spot position in London and are short futures on the COMEX. When a refinery in Switzerland, for example, casts big bars (400-ounce) and sells them to a bullion bank in London, the bank hedges itself on the COMEX. This makes the bank long spot and short futures.

金砖银行通常持有伦敦黄金现货,同时持有纽约黄金期货合约的空仓。举个例子,当瑞士的一家黄金精炼厂生产出一批400盎司重的金块并卖给一家伦敦的金砖银行,这家银行会在纽约黄金期货交易所COMEX卖出相应的黄金期货合约进行对冲。

“Exchange For Physical” (EFP) is an OTC swap. On the COMEX website it reads:

“期货转现货”是一种在场外进行的互换交易,在纽约黄金期货交易所COMEX的网站上可以看到相关的定义:

Exchange For Physical (EFP) allows traders to switch Gold futures positions to and from physical [spot], unallocated accounts. Quoted as dollar basis, relative the current futures prices, EFP is a key component in pricing OTC spot gold.

(The London Bullion Market is an OTC market.)

伦敦金条市场就是一个场外交易场所。

An EFP is usually a swap between a futures and a spot position. In banking jargon the word “EFP” also refers to, (i) having a position in both markets, and (ii) the spread in general (because the price of the EFP is equal to the difference in price between New York futures and London spot). A bullion bank that is “short EFP” is long spot and short futures.

“期货转现货”的交易通常是对期货和现货进行互换,“期货转现货”用银行的行话说指的是:1、在期货和现货市场上均持有头寸;2、通常是一种价差,因为“期货转现货”的报价等于纽约黄金期货合约的报价与伦敦现货金价之间的差价。如果一家金砖银行持有的是“期货转现货”的空头头寸,那么该行在做多黄金现货并做空黄金期货。

As mentioned, banks are most of the time short EFP. When the spread widened their short EFP starting bleeding. To avoid further losses, some banks “were forced to cover,” which added fuel to the fire. (It can also be the banks themselves started the spread to widen.) Many banks suffered severe losses.

前面提到,商业银行在大多数情况下持有的是“期货转现货”的空头头寸。当价差扩大,这些“期货转现货”的空头头寸开始产生亏损。为避免亏损加大,一些商业银行不得不平仓,这就好比火上浇油,很多银行会因此损失惨重。

Currently, most refineries in Switzerland have reopened. So, why does the spread persist? After all, arbitragers can hire planes to transport gold to wherever. On April 30, 2020, the spread was still $15 dollars per troy ounce.

现在,大多数瑞士的黄金精炼厂已经复工了。那么,为啥差价并未消除?毕竟,套利者可租飞机把黄金运到任何一个地方。2020年4月30日,纽约黄金期货合约的报价与伦敦现货金价之间的差价仍然高达15美元/盎司。

Because I couldn't figure this out myself, I asked John Reade, Chief Market Strategist of the World Gold Council, and Ole Hansen, Head of Commodity Strategy at Saxo Bank, for their views.

我搞不懂咋回事,因此向世界黄金协会的首席市场分析师John Reade以及盛宝银行大宗商品策略主管Ole Hansen请教。

Reade wrote me:

Reade是这么回复的:

I guess for two reasons: firstly, banks and traders probably still have large EFP positions that they haven’t been able to cover. And secondly, I doubt that risk officers and banks are prepared to allow large EFP positions to be run, so the usual arbitragers of this market cannot add to their positions, flattening the spread.

“我猜是出于两个原因:首先,商业银行和黄金交易员可能还有大量“期货转现货”的空头头寸无法平仓;其次,我认为负责风险管理的人员和商业银行打算允许大量“期货转现货”的空头头寸存在下去,因此市场上的套利者无法加仓抹平黄金期货和现货之间的价差。”

Which is in line with what Hansen wrote me:

Hansen的回复如下:

While COMEX has now allowed the delivery of 400oz bars (the most popular bar size in London) and raised spot positions limits the problem has not gone away. This means that the mechanism that should balance the gold market still isn’t functioning correctly despite improving underlying physical conditions.纽约黄金期货交易所COMEX现在允许交割400盎司重的金块(这是伦敦现货市场上最常见的黄金实物)并提高了现货黄金的持仓限额,但问题并没有化解。这意味着尽管黄金现货市场的状况有了改善,抹平黄金期货和黄金现货之间价差的机制并没有正常发挥作用。 Market makers [banks] have suffered major losses last month and as they tend to natural short the EFP (long OTC, short futures) the risk appetite and ability to drive it back to neutral has for now been disrupted.做市商(通常是商业银行)在上个月蒙受了巨额损失,他们的黄金仓位一般是做多黄金现货加做空黄金期货,因此当前其风险偏好和将黄金期货和黄金现货之间的价差推回正常水平的能力出了问题。

Banks lost so much money, they are cautious not to lose more. They don’t access funds to close the spread.

商业银行的损失是如此之大,他们很怕亏损额会增加,他们得不到足够的融资用套利的方式抹平差价。

Conclusion

结论

Generally, just the threat of delivery keeps markets in line as well. Any trader that sees an arbitrage opportunity can take position without the intention of making/taking delivery, in the knowledge that New York futures and London spot will converge. Now this certainty doesn’t prevail, traders are cautious. If they take positions but the spread widens, they lose.

一般来讲,正是有可能的现货交割使得期货和现货市场的报价保持一致。任何一个看到套利机会的交易员在开仓的时候都没打算进行实物交割,并带着伦敦现货金价和纽约黄金期货合约的报价终有一日会走到一起的想法。

Another reason why the spread can persist, is because of strong demand in New York. Speculators that reckon the price of gold will go up will buy long futures, increasing the spread. Normally, this type of demand is smoothly translated into the spot market by arbitragers without increasing the spread. But not now.

黄金期货和黄金现货之间的价差会持续存在的另一个原因是,纽约市场对黄金的需求非常强劲。投机者认为金价会上涨而做多纽约黄金期货合约,因此推高了价差的水平。正常情况下,对黄金的这种强劲需求会被套利者平顺地传导到现货市场的报价上且不会推高期货和现货之间的价差,但这次可不一样了。

In a nutshell, I think that logistics and credit restrictions prevent the spread to close. However, if anyone has a better analysis please comment below.

简而言之,我认为是物流中断和融资受限导致黄金期货和现货之间的价差无法被抹平。但如果谁有更好的解释,请告诉大家。

Addendum

补充几句

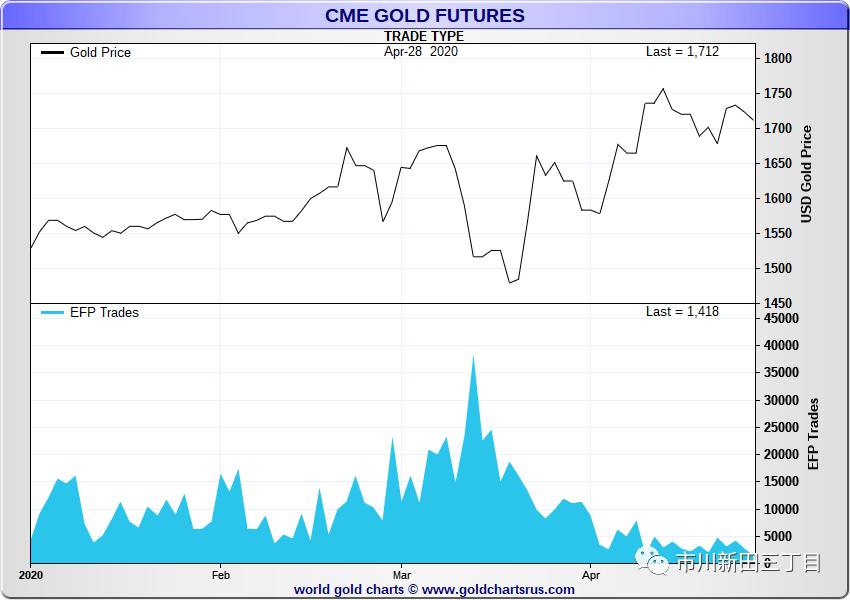

It can be, as John Reade wrote me, “banks and traders probably still have large EFP positions that they haven’t been able to cover.” I noticed on Nick Laird’s website Goldchartrus.com that EFP volume cleared through CME’s ClearPort is decreasing since early March, to levels not seen in a long time.

情况有可能像John Reade写给我的,“商业银行和交易员可能仍持有大量无法被平仓的期货转现货头寸。”我注意到Nick Laird的网站Goldchartrus.com上显示,通过芝加哥商品交易所的ClearPort系统清算的黄金期货转现货的交易量自三月初以来一直在减少,如今的成交量之低已经很长时间没见过了。

Perhaps this is a reflection of a market that is slowly trying to heal itself. Perhaps when all losses have been crystalized, banks, or other financial entities with sufficient firepower to hire planes etc., will close the spread.

也许这反映的是市场正在慢慢地试图自我修复,也许当所有的损失都被消化掉后,在商业银行或其他有能力雇得起航班的金融机构的努力下,黄金期货和现货之间的价差会被抹平。

Another possibility is that when the new COMEX futures contract—that can be delivered in 400-ounce bars—becomes active, the spread closes. At the time of writing, the open interest of this contract is virtually zero. Time will tell.

还有一个可能性是,当纽约黄金期货交易所COMEX新的黄金期货合约(可交割400盎司重的金块)变得成交活跃后,黄金期货和现货之间的价差会被抹平。在写这篇文章的时候,该合约的持仓量还几乎为零。拭目以待吧。